What is Stock Buyback?

A Stock Buyback occurs when a company decides to repurchase its own previously issued shares either directly in the open markets or via a tender offer.

What is the Definition of Stock Buyback?

A stock buyback, or “share repurchase,” is a corporate event wherein shares previously issued to the public and traded in the open markets are bought back by the original issuer.

Once a company repurchases a portion of its shares, the total number of shares outstanding (and available for trading) in the market is subsequently reduced post-buyback.

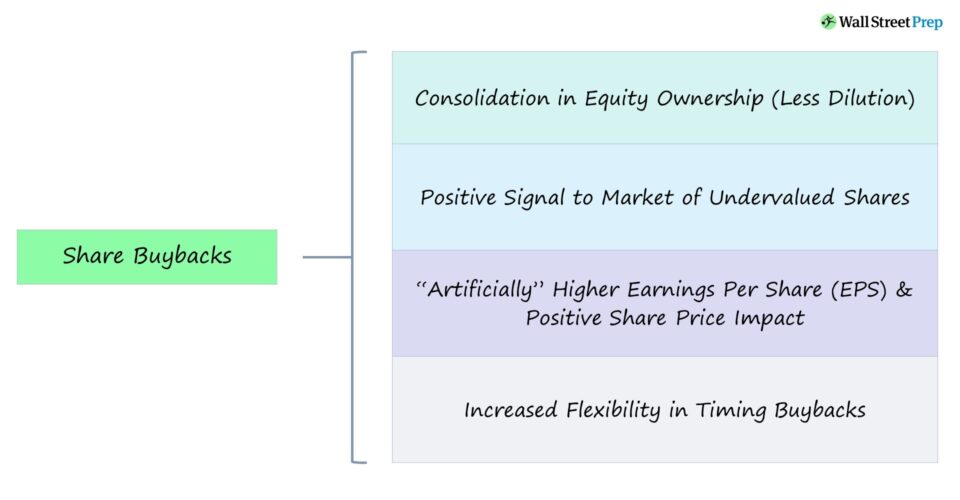

Stock buybacks often demonstrate that the company has sufficient cash set aside for near-term spending and point to management’s optimism about upcoming growth, resulting in a positive share price impact.

Since the proportion of shares owned by existing investors increases post-repurchase, management is essentially betting on itself by completing a buyback.

In other words, the company might believe its current share price (and market capitalization) is undervalued by the market, implying a stock buyback is a profitable move.

How Does a Stock Buyback Work?

The share price impact, in theory, should be neutral, as the share count reduction is offset by the decline in cash (and equity value).

Sustainable, long-term value creation stems from growth and operational improvements – as opposed to just returning cash to shareholders.

Yet, share buybacks can still affect a company’s valuation, either positively or negatively, contingent on how the market as a whole perceives the decision.

- Positive Stock Price Impact → If the market incorrectly under-priced the cash a company owns in the valuation, the buyback can cause a higher share price.

- Negative Stock Price Impact → If the market views the buyback as a last resort, signaling that the company’s pipeline of investments and opportunities is running out, the net impact is likely negative.

The stock buyback can benefit a company’s shareholders because of the increase in earnings per share (EPS) – both on a basic EPS and diluted EPS basis.

The core issue here, however, is that no real value has been created (i.e., the company’s fundamentals remain unchanged post-buyback).

Nevertheless, the implied share price projected by the price-to-earnings ratio (P/E) can increase post-buyback.

The Wharton Online & Wall Street Prep Applied Value Investing Certificate Program

Learn how institutional investors identify high-potential undervalued stocks. Enrollment is open for the Feb. 10 - Apr. 6 cohort.

Enroll TodayStock Buyback vs. Dividend: What is the Difference?

Share purchases are one method for companies to compensate shareholders, with the other option consisting of dividend issuances.

The difference between share buybacks and dividend issuances is that, rather than equity shareholders receiving cash directly, repurchases consolidate equity ownership (i.e., reduce dilution).

The reduction in dilution of ownership can indirectly create shareholder value post-repurchase.

One reason companies prefer share buybacks is to avoid the “double taxation” associated with dividends, in which the dividend payments are taxed twice:

- Corporate Level (i.e., Dividends are NOT Tax-Deductible)

- Shareholder Level

Many companies also pay employees using stock-based compensation to conserve cash, so the net dilutive impact of those securities can be partially (or entirely) counteracted by buybacks.

Once implemented, dividends are rarely cut unless deemed necessary.

Why? The market tends to assume the worst and expects future earnings to decrease if a long-term dividend program is abruptly cut, causing a sharp decline in share price.

Conversely, share repurchases are often one-time events.

Real-Life Stock Buyback Example: Apple (AAPL)

In the past decade, there has been a substantial shift towards share buybacks instead of dividends, as certain companies attempt to take advantage of their undervalued stock issuances while others strive to increase their stock price artificially.

The announcement of a long-term dividend program is interpreted as a statement that the company is now mature with fewer investments/projects to put its earnings to use.

Particularly among high-growth companies in the tech sector, most thereby opt for buybacks in lieu of dividends as buybacks send a more optimistic signal to the market regarding future growth prospects.

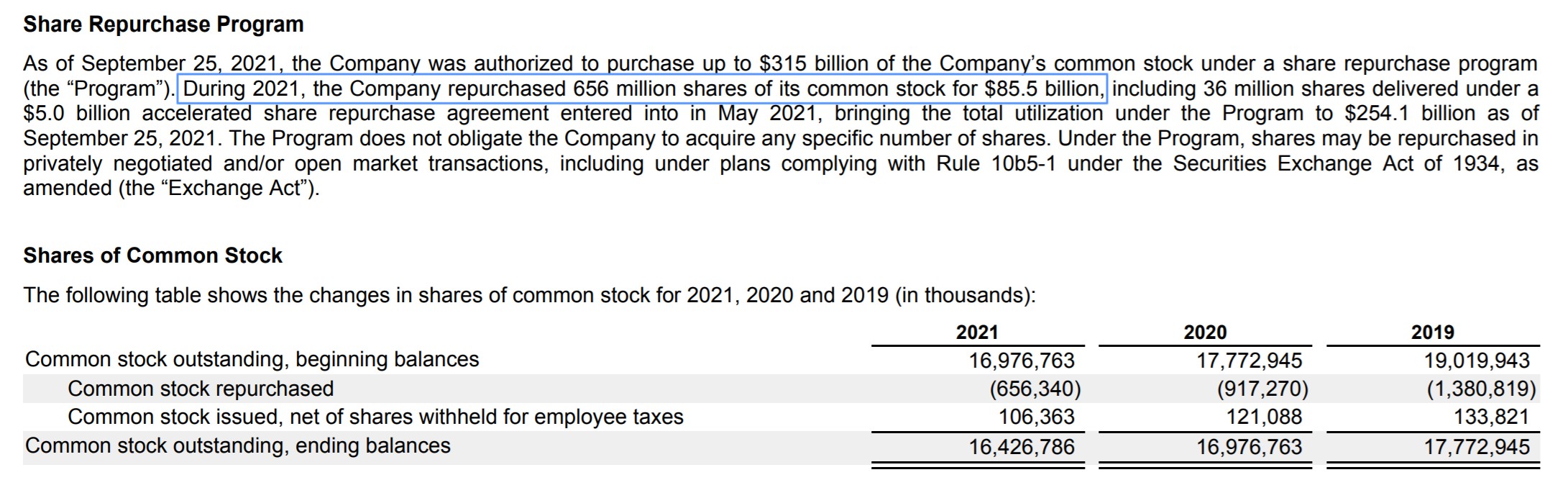

For example, Apple (NASDAQ: AAPL) has led all companies in the S&P 500 in the amount spent on share buybacks. In 2021, Apple spent $85.5 billion on share repurchases and $14.5 billion on dividends – as its market capitalization briefly touched $3 trillion in 2022.

Apple Share Repurchase Program (Source: AAPL FY 2021 10-K)

Stock Buyback Calculator

We’ll now move to a modeling exercise, which you can access by filling out the form below.

Stock Buyback Calculation Example

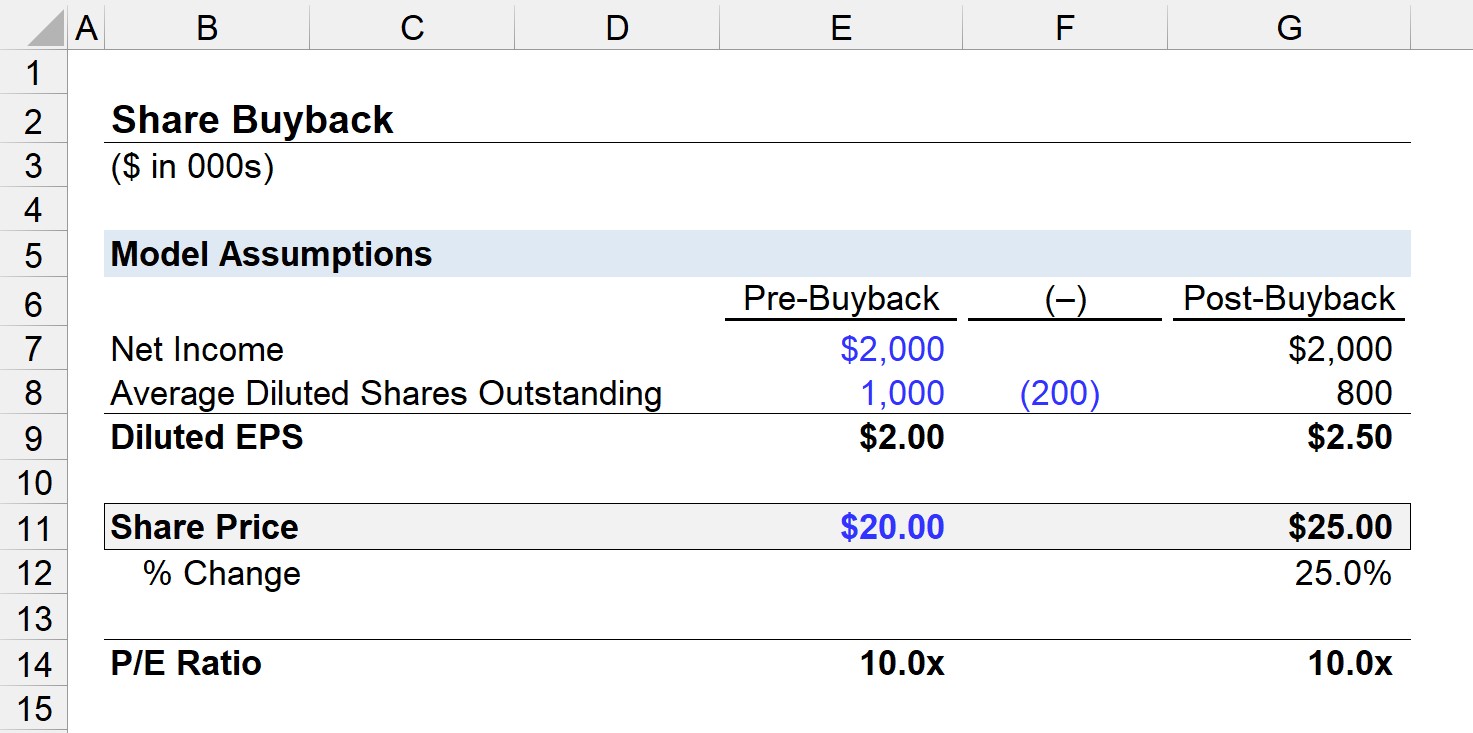

Suppose a company generated $2 million in net income and has 1 million shares outstanding prior to completing a stock buyback.

With that said, the diluted EPS pre-buyback is equal to $2.00.

- Diluted EPS = $2m ÷ 1m = $2.00

Moreover, we will assume the company’s share price was $20.00 on the date of the repurchase, so the P/E ratio is 10x.

- Price to Earnings (P/E Ratio) = $20.00 ÷ $2.00 = 10.0x

If the company repurchases 200k shares, the outstanding post-buyback number of diluted shares is 800k.

Given the $2 million in net income, the post-buyback diluted EPS equals $2.50.

- Diluted EPS = $2m ÷ 800k = $2.50

To maintain the 10x P/E ratio, the implied share price would be $25.00, which we calculated by multiplying the new diluted EPS figure by the P/E ratio.

- Implied Share Price = $2.50 × 10.0x = $25.00

- % Change = ($25.00 ÷ $20.00) – 1 = 25%

In our example scenario, there is, in fact, a positive share price impact, with the underlying cause of artificial inflation in EPS.

The accounting treatment on the balance sheet is shown below.

- Cash is credited by $4 million ($20.00 Share Price × 200k Shares Repurchased).

- Treasury Stock is debited by $4 million.

While the total shareholders’ equity on the balance sheet declines, there are fewer claims on the remaining equity.

If you have a share buyback that is a liquidity event for employees of a private company, is the liquidity event itself considered stock-based compensation? Trying to understand if appropriate for including in “adjusted EBITDA.” Thanks!