- What is the Paper LBO?

- Paper LBO Tutorial: Practice Training Guide

- How to Complete the Paper LBO

- Illustrative Paper LBO Prompt

- Paper LBO Example — Excel Template

- 1. Input Transaction and Operating Assumptions

- 2. Build Sources and Uses of Funds Table

- 3. Financial Forecast

- 4. Calculate Free Cash Flow (FCF)

- 5. LBO Exit Valuation and Return Metrics (IRR and MOIC)

What is the Paper LBO?

The Paper LBO is a common exercise completed during the private equity interview process, for which we’ll provide an example step-by-step practice test along with a walkthrough of each of the core concepts.

Paper LBO Tutorial: Practice Training Guide

Starting off, the interviewee typically receives a “prompt” – a short description containing a situational overview and certain financial data for a hypothetical company contemplating an LBO.

The interviewee will be given a pen and paper and between 5 and 10 minutes to arrive at the implied internal rate of return (IRR) and multiple on invested capital (MOIC) based on the information presented in the prompt.

For practically all private equity interviews, do not expect the interviewer to hand you a calculator, because only a pen and paper will be provided. In fact, the entire paper LBO test could even be a verbal discussion with the interviewer.

Therefore, practice completing mental math in your head until you are comfortable performing shorthand calculations, even under timed pressure.

Most private equity firms – or, in some cases, even headhunters (i.e. the “gatekeepers” of the industry) – use the paper LBO test as a method to quickly vet a potential candidate in the early stages of the PE interview process.

As candidates progress to subsequent rounds, private equity firms often ask interviewees to complete a far more detailed LBO modeling test, or perhaps even a take-home case study.

How to Complete the Paper LBO

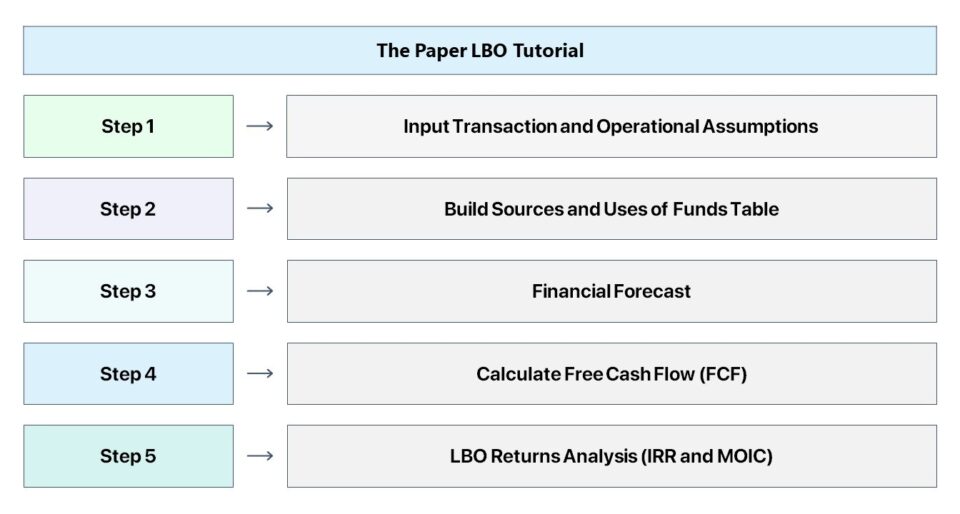

Before we begin, the steps to complete a paper LBO test are outlined below.

- Step 1 ➝ Input Transaction and Operating Assumptions

- Step 2 ➝ Build Sources and Uses of Funds Table

- Step 3 ➝ Financial Forecast

- Step 4 ➝ Calculate Free Cash Flow (FCF)

- Step 5 ➝ LBO Returns Analysis (IRR, MOIC)

The Wharton Online and Wall Street Prep Private Equity Certificate Program

Level up your career with the world's most recognized private equity investing program. Enrollment is open for the Feb. 10 - Apr. 6 cohort.

Enroll TodayIllustrative Paper LBO Prompt

To get started, the following is an example prompt for our practice paper LBO test.

Paper LBO Prompt Example

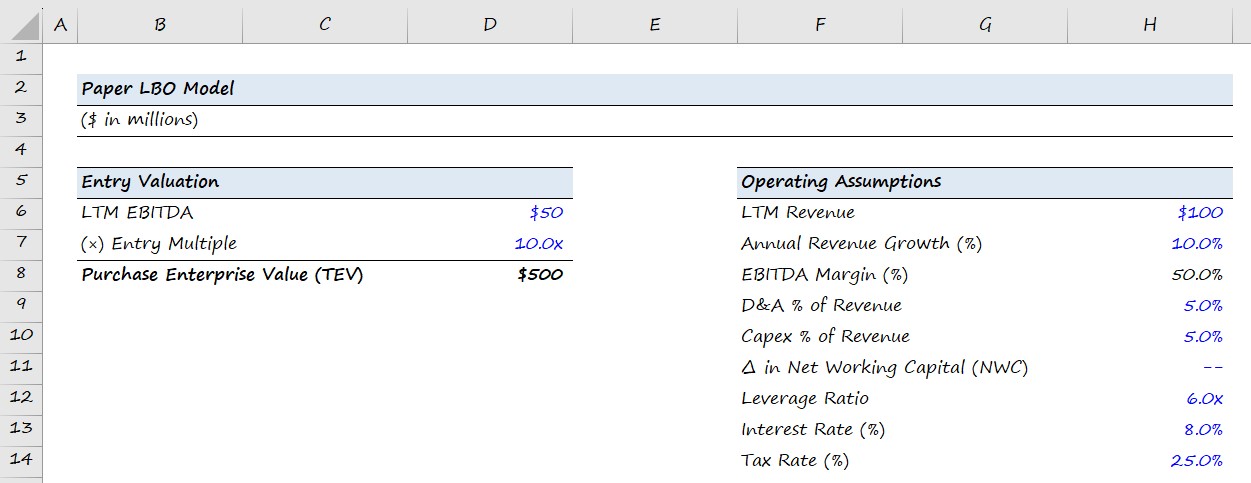

JoeCo, a coffee company, has generated $100mm in last twelve months (LTM) revenue and this figure is expected to increase by a growth rate of 10% annually into the foreseeable future.

JoeCo’s LTM EBITDA was $50mm, and its EBITDA margin should remain unchanged in the years ahead.

Based upon management guidance, JoeCo’s depreciation and amortization (D&A) and its capital expenditures (Capex) is expected to be 5.0% as a percentage of revenue, with no change in net working capital (NWC) and the effective tax rate fixed at 25%.

If a PE firm acquired JoeCo for 10.0x EBITDA and exited at the same multiple five years later, what is the implied internal rate of return (IRR) and multiple on invested capital (MOIC)?

For the financing of the LBO, assume the initial leverage ratio used to fund the purchase was 6.0x EBITDA and that the debt carries an interest rate of 8.0% with no required principal amortization until maturity, at which debt is fully paid down upon exit.

Paper LBO Example — Excel Template

Fill out the following form to access the paper LBO template, which we recommend using to confirm your calculations are correct.

However, it is rather unlikely that you’ll receive a laptop with Excel in the interview setting, nor a calculator.

Therefore, print out the 1st sheet to solve this problem set and complete the exercise using pen and paper to practice under the actual testing conditions.

1. Input Transaction and Operating Assumptions

The first step is to lay out the operational assumptions that were provided in the prompt and to calculate the total amount paid to purchase the target company.

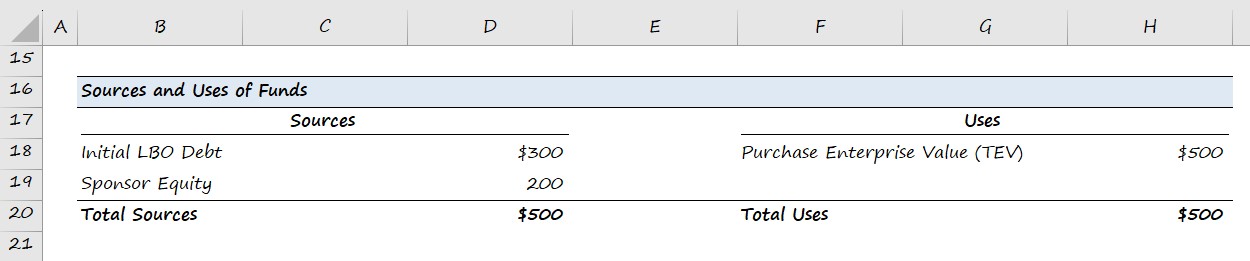

2. Build Sources and Uses of Funds Table

In the next step, we will build the Sources and Uses table, which will be a direct function of the transaction structure assumptions. In this particular example, the purchase multiple used was 10.0x EBITDA, and the deal was funded using 6.0x leverage.

More specifically, the objective of this section is to figure out the exact cost of purchasing the company, and the amount of debt and equity financing required to complete the acquisition.

The total amount of debt used will be calculated as a multiple of LTM EBITDA, while the equity contribution by the private equity investor is the remaining amount required to “plug” the gap and make both sides of the table balance.

Ultimately, the main goal of an LBO model is to determine how much the firm’s equity investment has grown. To do so, we need to first calculate the size of the initial equity check by the financial sponsor.

In a real LBO model, the Uses of Funds Section will likely include transaction and financing fees, among other uses. In addition, other more complex concepts like management rollover will be reflected in both the sources and uses of funds.

However, these nuances are unlikely to show up here, so unless you were explicitly provided with additional data in the prompt, focus exclusively on the data provided.

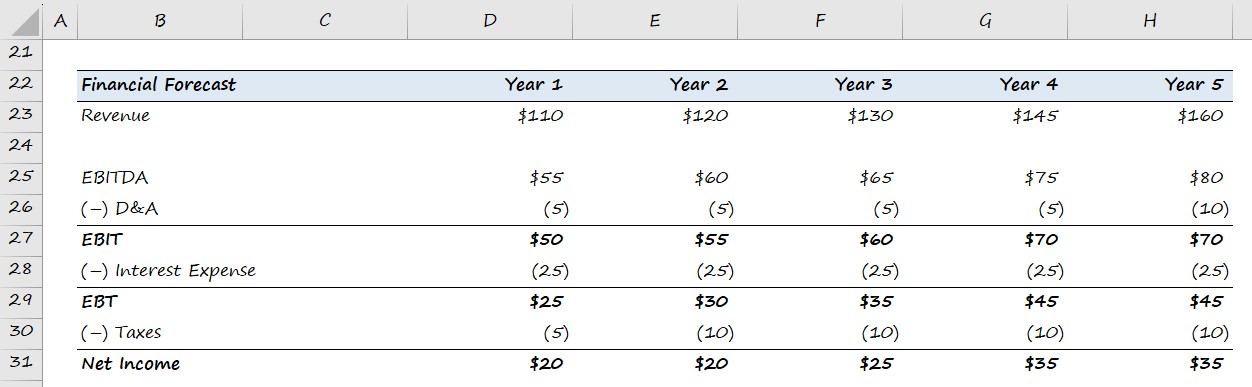

3. Financial Forecast

Since we have completed the Sources and Uses of Funds section of our LBO model, we will shift to forecasting the financials of JoeCo from revenue to net income (the “bottom line”).

The operational assumptions that will drive the projections were provided in the first step.

Note: In the context of a private equity interview, it is reasonable to round your calculations to the nearest whole number for convenience, i.e. round the figures to the nearest 5 or 10 to simplify the math.

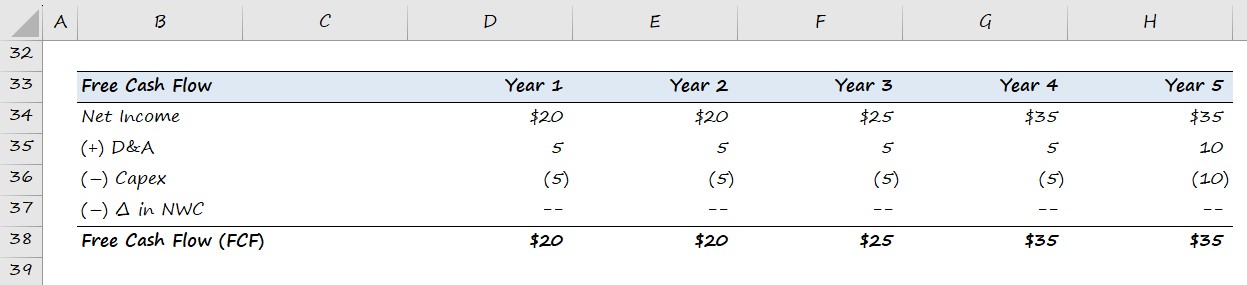

4. Calculate Free Cash Flow (FCF)

With our financial forecast complete, we can now calculate JoeCo’s free cash flows (FCFs) throughout the five-year holding period.

The FCF generation of an LBO target determines the amount of debt that can be paid down during the holding period. However, our prompt mentioned assumes no principal paydown.

Free Cash Flow (FCF) = Net Income + D&A – Capex – Change in NWC

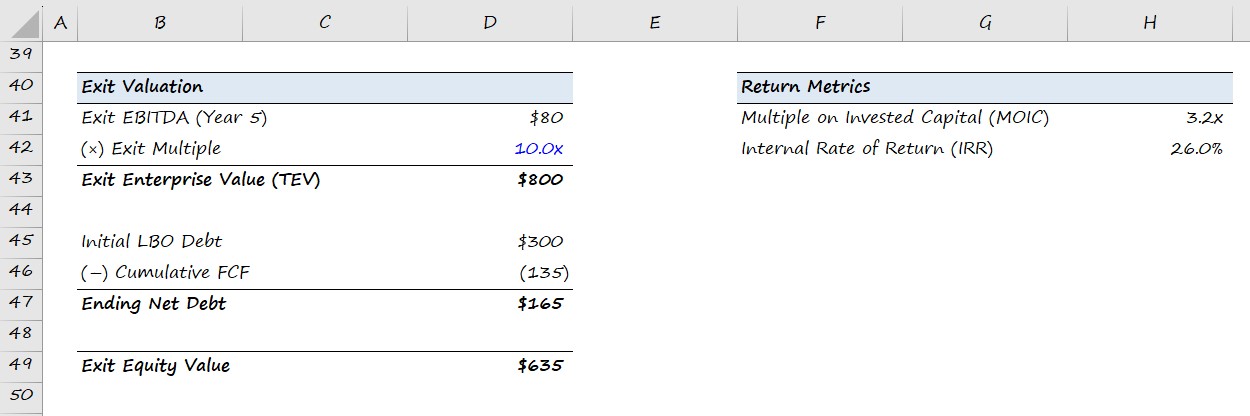

5. LBO Exit Valuation and Return Metrics (IRR and MOIC)

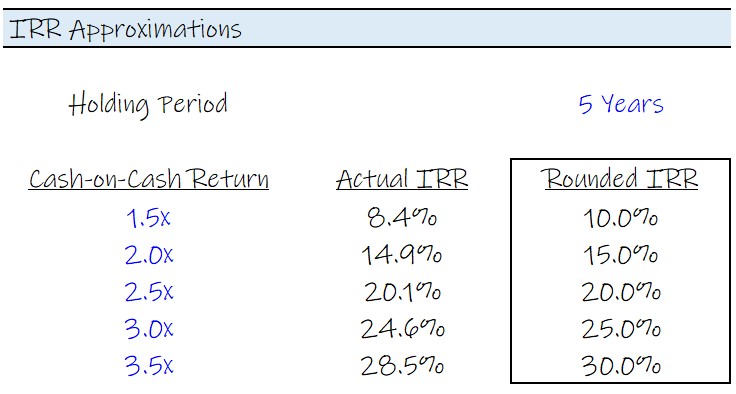

In the last step, we will assess the returns of the investment using the multiple on invested capital (MOIC), or “cash-on-cash return”, and the internal rate of return (IRR).

Earlier, the prompt stated the PE firm exited the investment at the same multiple as the entry multiple (i.e. no “multiple expansion”).

Since you will likely not have access to a calculator, calculating the IRR requires some “back-of-the-envelope” math.

The standard investment holding period assumption is 5 years, so we recommend memorizing the IRR approximations based on the most common MOIC returns.

The Rule of 72 in Paper LBOs

Forgot your IRR approximations?

No problem — in most cases, the return should be easy to approximate under the Rule of 72, which estimates the time that it takes to double an investment.

The approximate number of years necessary for the investment value to double in size can be determined by dividing 72 by the rate of return.

For example, over a 5-year horizon, the approximate IRR required to double the investment is ~15%.

- Number of Years to Double = 72 ÷ 5 = ~15%

There’s also the lesser-known Rule of 115, which estimates the time it takes to triple an investment. Here, the formula takes 115 and divides it by the rate of return.

If you are facing difficulty estimating the internal rate of return (IRR), it is likely that a mistake was made in one of the prior steps.

The implied MOIC in our hypothetical LBO scenario is around 3.2x, which we calculated by dividing the exit equity value by the initial sponsor equity contribution.

Using either the table above or the Rule of 72 and 115, we can estimate the internal rate of return (IRR) on our hypothetical LBO investment to be approximately ~26%.

- Multiple on Invested Capital (MOIC) = 3.2x

- Internal Rate of Return (IRR) = 26.0%

Wouldn’t you acquire the company on an NTM EBITDA number?

Hey, why did the D&A and Cap Ex not increase as a % of the increasing revenue? Why did the real figures stay constant at 5?

Does this get you to levered or unlevered FCF?

I just completed this paper LBO – Thank you. In how long should this paper LBO need to have been completed?

Why isn’t cash taxes accounted for in the FCF walk?

You can also estimate the IRR by using the Rule of 40M, where the IRR is [40 * M / No. of Years]. It works for MOIC and holding years that are not whole numbers. In the example above (3.2x in 5 years), the IRR would be 40*3.2/5 >> 26%.… Read more »

Hey, So for the EBITDA LTM it’s the EBIT LTM – D&A LTM ?