- What is a Prospectus?

- How Does a Prospectus Work in Finance?

- What are the Different Types of Prospectus Filings?

- What is the Purpose of the IPO Prospectus?

- S-1 vs. S-3 Prospectus Filing: What is the Difference?

- What are the Sections of a Prospectus Filing?

- IPO Prospectus Example: Coinbase S-1 Filing (PDF)

- How to Read a Prospectus Filing?

What is a Prospectus?

A Prospectus is a formal document filed with the Securities and Exchange Commission (SEC) by companies intending to raise capital by offering securities to the public.

How Does a Prospectus Work in Finance?

The prospectus filing, often used interchangeably with the term “S-1”, contains all the necessary details about a public company’s proposed offering in order to help investors make an informed investment decision.

The prospectus is a mandatory part of the registration process for a new share issuance in the U.S., i.e. an initial public offering (IPO).

The topics covered in the prospectus include the nature of the business, the company’s origins, the background of the management team, historical financial performance, and the company’s anticipated growth outlook.

What are the Different Types of Prospectus Filings?

There are two primary types of prospectus documents that companies put together during the process of raising capital.

- Preliminary Prospectus → The preliminary prospectus, or “red herring”, provides prospective institutional investors with information regarding an upcoming IPO but is less formal, and there is still time for changes to be implemented based on the initial feedback received.

- Final Prospectus → The final prospectus, or the “S-1”, is the version filed with the SEC for final approval. Compared to the preliminary prospectus that preceded it, this document is far more detailed and is meant to be the “official” filing right before a new offering of securities is completed.

The preliminary prospectus comes before the S-1 filing and is circulated among institutional investors during the “quiet period” until the registration becomes official with the SEC.

What is the Purpose of the IPO Prospectus?

The purpose of the preliminary prospectus is to gauge investor interest and adjust terms if deemed necessary, i.e. its function is similar to that of a marketing document.

Once the company and its advisors are prepared to issue new securities to the public, the final prospectus is submitted.

The final prospectus — a more complete document with changes implemented based on feedback from investors and the SEC — is far more in-depth than the red herring.

Often, SEC regulators can request specific material to be added to the document to ensure there are no missing pieces of information that could potentially mislead investors.

Before the company in question can proceed with its planned IPO and distribution of new shares, the official final prospectus must first be filed with formal approval from the SEC.

S-1 vs. S-3 Prospectus Filing: What is the Difference?

If a company is issuing securities to the public markets for the first time, the S-1 regulatory document must be filed with the SEC.

But if we suppose an already-public company intends to raise more capital, the far less time-consuming and simplified S-3 report would be filed instead.

- S-1 Filing → Initial Public Offering (IPO)

- S-3 Filing → Secondary Offering (Post-IPO)

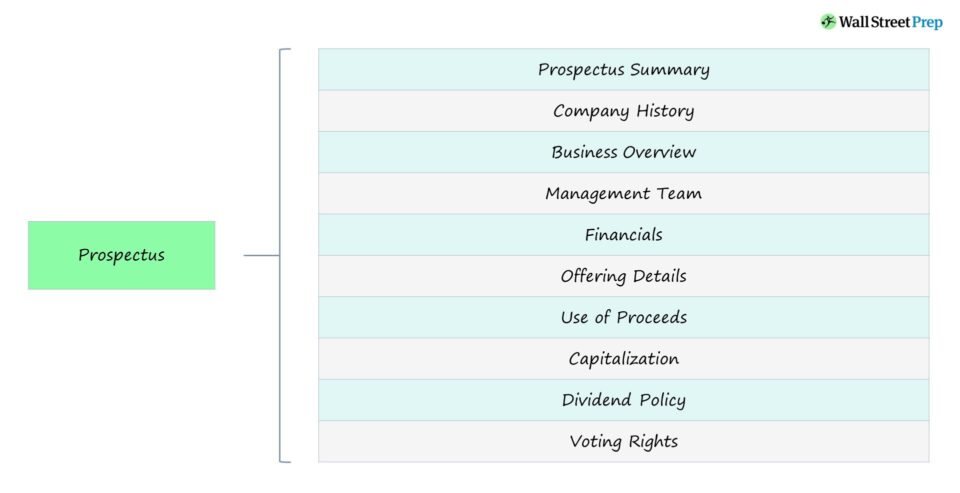

What are the Sections of a Prospectus Filing?

The table below summarizes the key components of a prospectus that investors (and the SEC) tend to pay the most attention to.

| Section | Description |

|---|---|

| Prospectus Summary |

|

| Company History |

|

| Business Overview |

|

| Management Team |

|

| Financials |

|

| Risk Factors |

|

| Offering Details |

|

| Use of Proceeds |

|

| Capitalization |

|

| Dividend Policy |

|

| Voting Rights |

|

IPO Prospectus Example: Coinbase S-1 Filing (PDF)

Each company’s S-1 report is unique, because the information considered “material” is specific to each individual company (and the industry it operates in).

An example of a prospectus filing can be viewed by filling out the form below. The S-1 was filed before the initial public offering (IPO) of Coinbase (NASDAQ: COIN) in early 2021.

How to Read a Prospectus Filing?

The table of contents (TOC) for Coinbase’s S-1 filing is as follows:

- A Letter from our Co-Founder and CEO

- Prospectus Summary

- Risk Factors

- Special Note Regarding Forward-Looking Statements

- Market and Industry Data

- Use of Proceeds

- Dividend Policy

- Capitalization

- Selected Consolidated Financials and Other Data

- Management’s Discussion and Analysis of Financial Condition and Results of Operations

- Business

- Management

- Executive Compensation

- Certain Relationships and Related Party Transactions

- Principal and Registered Stockholders

- Description of Capital Stock

- Shares Eligible for Future Sale

- Sale Price History of our Capital Stock

- Certain Material U.S. Federal Income Tax Consequences to Non-U.S. Holders of Our Common Stock

- Plan of Distribution

- Legal Matters

- Change In Accountants

- Experts

- Additional Information

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today