What is Lessor vs. Lessee?

The Lessor vs. Lessee difference is that the lessor lends an asset, such as equipment or property, to the lessee in exchange for periodic interest payments throughout the borrowing term.

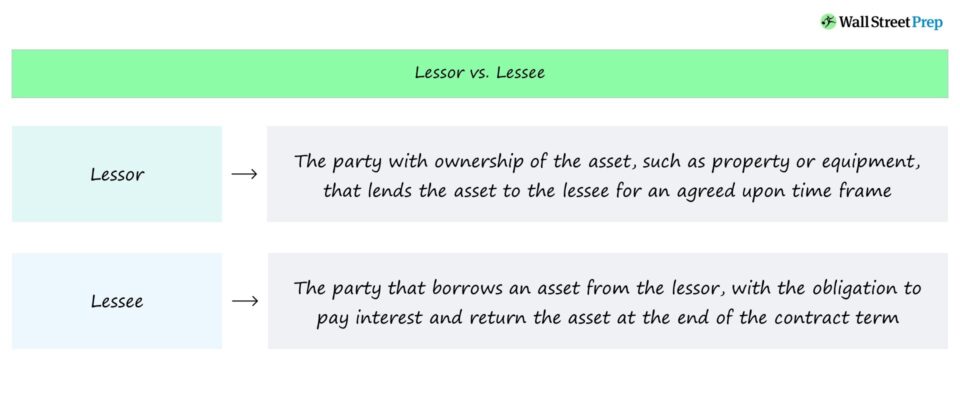

Lessor vs. Lessee: Roles in Real Estate Lease Agreement

There are two parties involved in a lease agreement: 1) the lessor and 2) the lessee.

- Lessor → The party with ownership of the asset that lends the asset to the lessee, or borrower, for a specified period.

- Lessee → The party that borrows an asset with the promise to pay interest to the lessor and return of the asset at the end of the contract.

The lease is a contractual, legally binding agreement between the two parties, where the lessor lends an asset for use by the borrower or lessee.

In exchange for the right to use the asset, the lessee must make periodic interest payments to the lessor throughout the borrowing term.

Once the maturity date per the lease agreement arrives, the lessee must return the borrowed asset to the lessor, or else there will probably be legal ramifications.

If applicable to the situation, the lessor can expect to receive compensation for any material losses related to damages to the asset.

Lessor vs. Lessee: What is the Difference?

The decision to lease an asset rather than purchase it outright can be more reasonable in terms of capital allocation, i.e., it is usually cheaper to lease than to purchase.

The assets involved in lease agreements are most often real estate properties, equipment, and machinery.

The usage of the borrowed asset is restricted, however, as any material changes, such as customization, must be approved by the lessor.

Suppose the borrowed asset is sold; the sale must receive authorization from the lessor before the transaction can be completed (and the proceeds are distributed to the lessor, with the exact split dependent on the contract terms).

The option for the lessee to purchase the asset will often also be offered at maturity.

The Wharton Online and Wall Street Prep Real Estate Investing & Analysis Certificate Program

Level up your real estate investing career. Enrollment is open for the Feb. 10 - Apr. 6 Wharton Certificate Program cohort.

Enroll TodayCapital Lease vs. Operating Lease: What is the Difference?

There are several types of lease agreements frequently seen in corporate finance, namely the following two structures:

- Capital Lease → A capital lease, or “finance lease,” describes a lease agreement where the lessee obtains ownership of the asset. Since the lessee possesses full control over the asset (and is responsible for any maintenance or associated ongoing costs), the accounting standards under GAAP require the lease agreement to be recorded on the lessee’s balance sheet as an asset with a corresponding liability, with interest expense recognized on the income statement.

- Operating Lease → An operating lease, on the other hand, is a lease agreement where the lessor continues to retain full ownership of the asset (and all associated considerations). The lessor remains responsible for any related costs of the asset, such as maintenance, rather than the lessee. Contrary to the accounting treatment of a capital lease, the asset is not recorded on the lessee’s balance sheet.

How Does a Sale and Leaseback Work?

Another common type of lease arrangement is called a “sale and leaseback,” which is a specific type of agreement whereby a buyer purchases an asset from another party intending to lease it right back to the seller.

The seller, in effect, becomes the lessee, while the buyer becomes the lessor post-transaction.

Once the ownership of the asset transfers, the seller leases the asset back from the buyer shortly afterward.

A sale-leaseback arrangement allows the seller to continue using the asset while improving its liquidity positioning (i.e., more cash on hand).