- What is Debt to Income Ratio?

- How the Debt to Income Ratio Works (DTI)

- How to Calculate Debt to Income Ratio (DTI)

- Debt to Income Ratio Formula (DTI)

- What is a Good Debt to Income Ratio?

- Debt to Income Ratio Calculator (DTI)

- 1. Monthly Debt and Income Calculation Example

- 2. Debt to Income Ratio Calculation Example (DTI)

- Front-End vs. Back-End DTI Ratio: What is the Difference?

What is Debt to Income Ratio?

The Debt to Income Ratio (DTI) measures the creditworthiness of a consumer by comparing their total monthly debt payment obligations to their gross monthly income.

How the Debt to Income Ratio Works (DTI)

The debt to income ratio (DTI) is a method to determine the ability of a borrower to satisfy all payment obligations associated with the financing arrangement.

If a higher proportion of a consumer’s monthly income must be spent on required debt payments, the likelihood of default and the credit risk to the lender are greater (and vice versa).

In practice, the debt to income ratio is most common among lenders to determine the creditworthiness of a potential borrower, i.e. analyze the default risk.

For a lender to achieve the expected return on a loan issuance (or related financing product), the borrower must reliably complete the required debt payments, namely the interest expense and the repayment of the original loan principal.

| Sources of Returns | Description |

|---|---|

| Interest Expense (Periodic Payments) |

|

| Loan Repayment (Principal Amortization) |

|

For example, an individual consumer who took out a mortgage to finance the purchase of a house must issue monthly payments to the bank lender until the mortgage is entirely paid off.

The receipt of the interest and principal is conditional on the borrower’s income being adequate to fulfill the payment obligations on time, per the lending agreement.

The lender must thereby make sure that the borrower can, in fact, manage the debt payments with a reasonable margin of safety.

Of course, external factors such as inflation can impact the real interest rates earned. However, the default risk of the borrower is a critical factor that lenders can use to quantify and mitigate the chance of incurring monetary losses.

How to Calculate Debt to Income Ratio (DTI)

The process of calculating a consumer’s debt to income (DTI) ratio can be broken into a four-step process:

- Calculate the Consumer’s Total Debt Payment Obligations Owed per Month

- Calculate the Consumer’s Gross Monthly Income (Unadjusted Pre-Tax Earnings)

- Divide the Consumer’s Monthly Debt Payments by the Gross Monthly Income

- Multiply by 100 to Convert the DTI Ratio into a Percentage

Debt to Income Ratio Formula (DTI)

The debt to income ratio formula compares the value of the anticipated monthly debt obligations to the borrower’s gross monthly income.

The DTI ratio is expressed as a percentage, so the resulting figure must be multiplied by 100.

If a consumer’s gross monthly income varies substantially month over month, the guidance is to use the income amount most representative of the consumer’s “typical” month, i.e. the normalized earnings generated by the consumer.

Because the lender is given access to the relevant income figures, it is in the consumer’s best interests to be conservative, especially if monthly income is enough.

The Wharton Online and Wall Street Prep Real Estate Investing & Analysis Certificate Program

Level up your real estate investing career. Enrollment is open for the Feb. 10 - Apr. 6 Wharton Certificate Program cohort.

Enroll TodayWhat is a Good Debt to Income Ratio?

Each lender sets its own specific benchmarks for what is a “good” debt to income (DTI) ratio. However, the table below outlines the general guidelines for interpreting the DTI ratio.

| DTI Ratio | Generalized Outcome | Description |

|---|---|---|

| <36% DTI |

|

|

| 36% to 42% DTI |

|

|

| 43% to 50% DTI |

|

|

| >50% DTI |

|

|

If the debt to income ratio (DTI) of a borrower is below 36%, most lenders deem the credit risk manageable.

However, other factors such as the consumer’s credit history, liquid assets on file, and the conditions of the credit market on the present date can still influence the lender’s final decision.

- Consumer Credit History

- Liquid Assets (Collateral)

- Credit Market Conditions

- Size of Borrowing (Loan)

- Length of the Borrowing Term

Generally speaking, lenders view consumers with lower DTI ratios more favorably and as more suitable borrowers, since the risk of default on the loan is lower (and vice versa for consumers with higher DTI ratios).

One caveat to a low DTI ratio, however, is that similar to a credit score, not having one presents a risk to lenders, since there is no track record of responsible credit management.

In effect, the formal recommendation by the Consumer Financial Protection Bureau (CFPB), under the context of mortgage financing, is to maintain a ratio of around 28% to 35% percent.

Debt to Income Ratio Calculator (DTI)

We’ll now move on to a modeling exercise, which you can access by filling out the form below.

1. Monthly Debt and Income Calculation Example

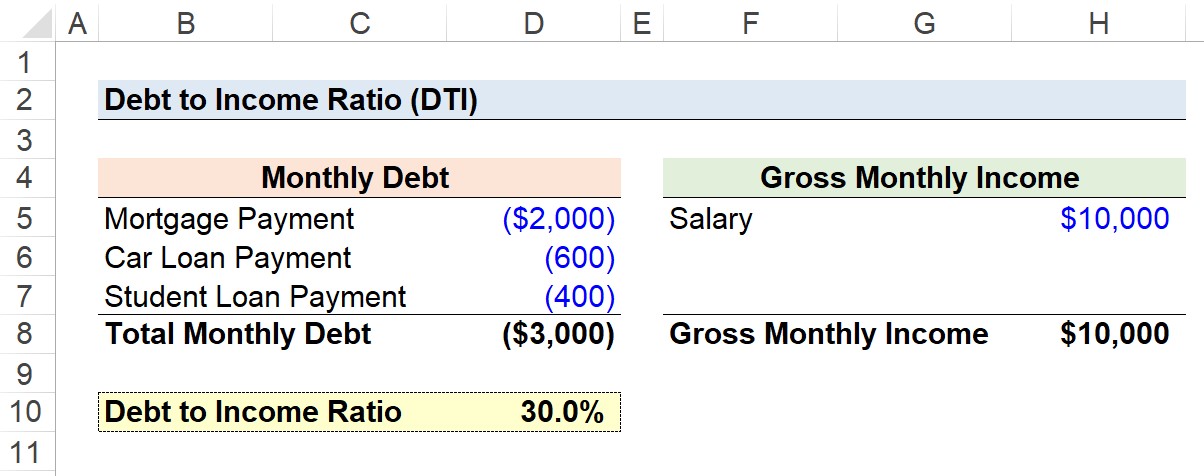

Suppose we’re tasked with calculating the debt to income ratio of a prospective borrower, to help determine the lending decision related to mortgage financing.

Starting off, we’ll calculate the consumer’s fixed debt payments, of which there are four.

- Mortgage Payment = $2,000

- Car Loan Payment = $600

- Student Loan Payment = $400

Thus, the total monthly debt of the consumer amounts to $3,000.

- Total Monthly Debt = $2,000 + $600 + $400 =$3,000

With our first input – the total monthly debt – complete, the next step is to calculate the consumer’s gross monthly income.

In our simple example, we’ll assume that our consumer’s gross monthly income is $10,000.

- Gross Monthly Income = $10,000

2. Debt to Income Ratio Calculation Example (DTI)

Since we have the two necessary inputs to calculate the debt to income ratio (DTI), the final step is to divide our consumer’s total monthly debt by their gross monthly income.

- Debt to Income Ratio (DTI) = $3,000 ÷ $10,000 = 0.30, or 30%

To reiterate from earlier, most lenders interpret a sub-36% DTI ratio as a strong credit profile and reliable borrower.

If the rest of the diligence conducted by the lender confirms the implied credibility of the borrower and the findings from the debt to income rate (DTI) calculation, our hypothetical borrower is likely to be approved for the mortgage.

Front-End vs. Back-End DTI Ratio: What is the Difference?

There are two variations of the DTI ratio that can impact which items should (or should not) be included in the calculation of the debt payments.

- Front-End DTI Ratio → The front-end DTI ratio compares the consumer’s gross income to only its housing costs, such as rental expenses, mortgage payments, and property insurance payments. Hence, the front-end DTI ratio is often used interchangeably with the term “housing ratio”.

- Back-End DTI Ratio → The back-end DTI ratio ignores all housing costs and instead compares the consumer’s gross income to other debt payments like student loans auto payments, credit card bills, court-mandated child support, alimony, and non-housing insurance payments.

In either case, note that only fixed, recurring debt payments are counted, rather than one-time costs not expected to continue.

Monthly expenses incurred day-to-day should also be excluded, such as spending related to purchasing groceries and utility bills (e.g. electricity, gas, and water).