What is a Cash Sweep?

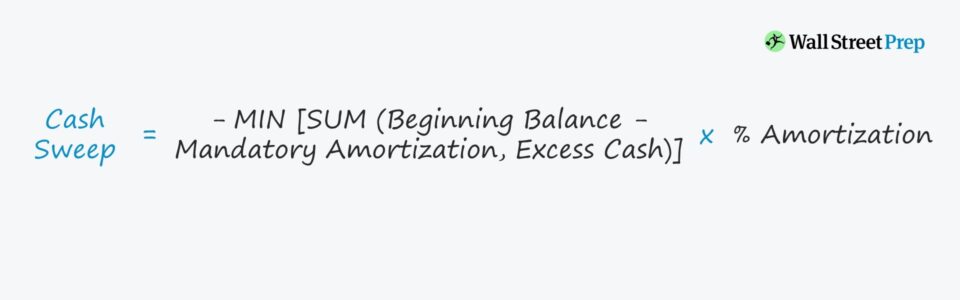

The Cash Sweep refers to the optional prepayment of debt using excess free cash flows in advance of the originally scheduled repayment date.

Once all mandatory payments have been met, a borrower can opt to pay down a portion of its outstanding debt earlier than anticipated with its excess cash (if any).

Cash Sweep: LBO Model Debt Schedule

The discretionary, early pay-down of debt reduces the principal balance coming due on the date of maturity – which decreases the credit risk of the borrower.

The reduction in debt principal also causes the interest expense (i.e. the periodic payments to the lender in exchange for the borrowing) to decline.

Certain debt providers such as senior lenders (e.g. corporate banks), who prioritize capital preservation above all else, will gladly accept early payment with either minimal (or no) early prepayment penalties imposed on the borrower.

In contrast, other returns-oriented lenders will typically issue debt with provisions prohibiting early prepayment, either for a specified period or for the entire duration of the loan.

Such lenders may also charge substantial prepayment penalties, even should early prepayment be allowed.

Modeling the Cash Sweep: LBO Optional Debt Paydown

In Excel, the formula for the cash sweep must calculate the free cash flow once all required payments are met, including the mandatory amortization of debt.

The excess cash is the amount remaining once all the following have been accounted for:

- “Rolled-Over” Excess Cash on the B/S from the Prior Period

- Cash Flow from Operations in the Current Period

- Cash Flow from Investing in the Current Period

- Cash Flow from Financing in the Current Period

If the borrower has remaining excess cash, the borrower can periodically pay down debt early – assuming the credit agreement does not contain language prohibiting such prepayments.

Additionally, the minimum cash balance of the company (i.e. the amount of cash required to be on hand by the company to fund working capital needs) must also be taken into consideration.

The Wharton Online and Wall Street Prep Private Equity Certificate Program

Level up your career with the world's most recognized private equity investing program. Enrollment is open for the Feb. 10 - Apr. 6 cohort.

Enroll TodayWhat are the Pros and Cons to LBO Debt Prepayment?

- Credit Profile: One of the key incentives for a company to opt for a cash sweep, other than lowering its interest expense burden, is to positively impact its credit profile – i.e. contributing to a lower debt-to-equity (D/E) ratio.

- Financial Stability + Debt Capacity: Early payment improves the company’s financial stability, as well as its ability to secure debt financing on a later date when cash is running low (or refinancing in a lower-interest-rate environment).

- Interest Tax Shield: One drawback, however, is that the reduced interest expense means the “tax shield” benefit of debt financing is also reduced (i.e. the tax savings caused by interest expense lowering taxable income). Thus, the borrower must weigh the pros and cons of using excess cash to pay down debt early, as the benefits of lower interest expense and reduced credit risk must outweigh any prepayment penalties incurred.

- Prepayment Restrictions: Lenders set different minimum return hurdles based on their risk tolerance among other various factors, so their willingness to permit cash sweeps and the associated fee structures tends to be very specific to each particular situation. The terms of the arrangement surrounding prepayments is outlined in the formal lending agreement between the borrower and the lender (e.g. bank, institutional investor).

- Prepayment Fee: By charging a prepayment penalty, the lender is protecting the yield on their debt and receiving compensation for reinvestment risk (i.e. the risk of finding another borrower), which offsets the interest expense savings of the borrower, As a result, bonds and riskier debt securities lower in the capital structure are costlier forms of debt financing.

LBO Cash Sweep Calculator

We’ll now move to a modeling exercise, which you can access by filling out the form below.

LBO Cash Sweep Calculation Example

The first step is to list out the model assumptions for our simple cash sweep exercise.

For purposes of simplicity, the “Excess Cash Available for Cash Sweep” line item is assumed to be $40m in all periods.

In reality, the free cash flow (FCF) amount – i.e. the cash available before optional debt repayments – is impacted by operating metrics such as revenue and EBITDA, as well as financing line items like mandatory amortization.

However, since modeling out an entire income statement and cash flow statement with a debt schedule would detract our attention away from the cash sweep concept, we’ll just extend the $40m FCF assumption for the entire projection.

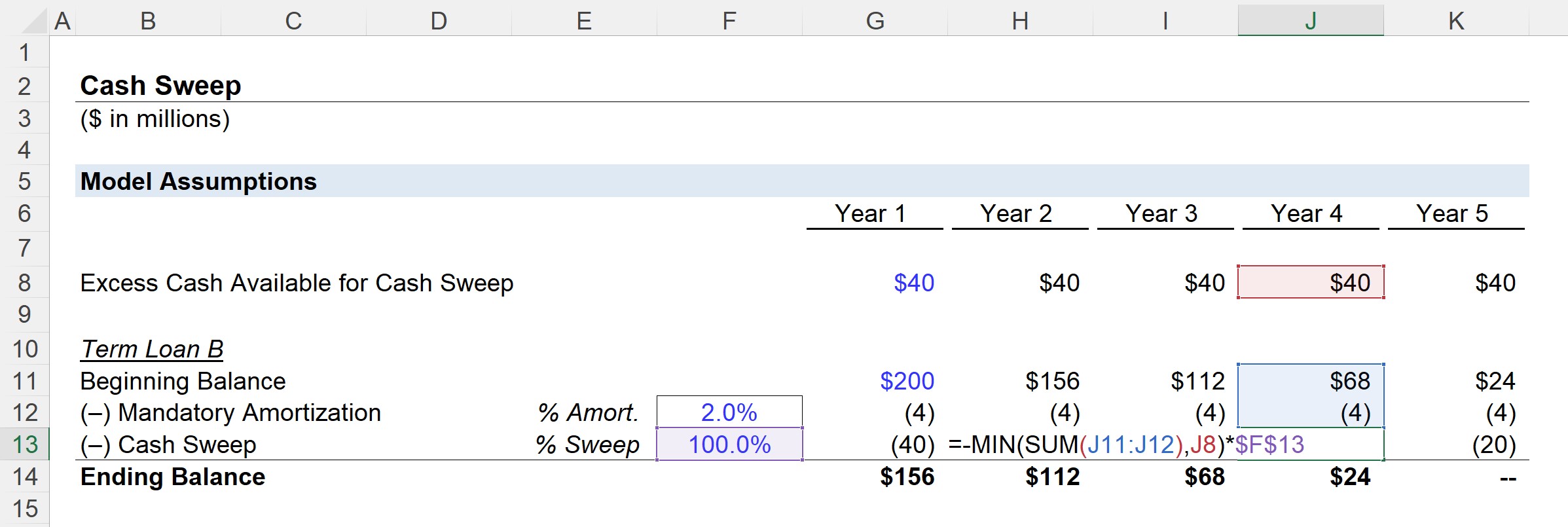

In our model example, our company has one tranche of debt – Term Loan B, with the borrowing arrangement lasting for 5 years.

- Beginning Balance (Year 1) = $200 million

- Mandatory Amortization = 2.0%

- Cash Sweep = 100.0%

From the first two assumptions, we can calculate the mandatory amortization by multiplying the 2.0% amortization assumption by the original principal amount – which comes out to $4m.

Under a contractual obligation, the borrower must repay 2.0% (or $4mm) of the original principal back to the lender to avoid defaulting.

Next, we’ll be assuming a full cash sweep – i.e. 100% of the excess cash goes towards repaying the principal balance. This is somewhat unrealistic, but we incorporate this into our exercise so that the effects of the cash sweep are more intuitive.

For instance, there is $40m in excess cash in Year 4 with a beginning term loan B balance of $68m.

- Beginning Term Loan B Balance – Year 4: $68m

- (–) Mandatory Amortization = $4m

- (–) Cash Sweep = $40m

In Year 4, the term loan B balance is $64m after deducting the mandatory amortization. The excess cash amounts to $40m – therefore, the cash sweep is also equal to $40m.

The formula for calculating the mandatory amortization can be found below – note the inclusion of the “MIN” function to prevent the ending balance from falling below zero.

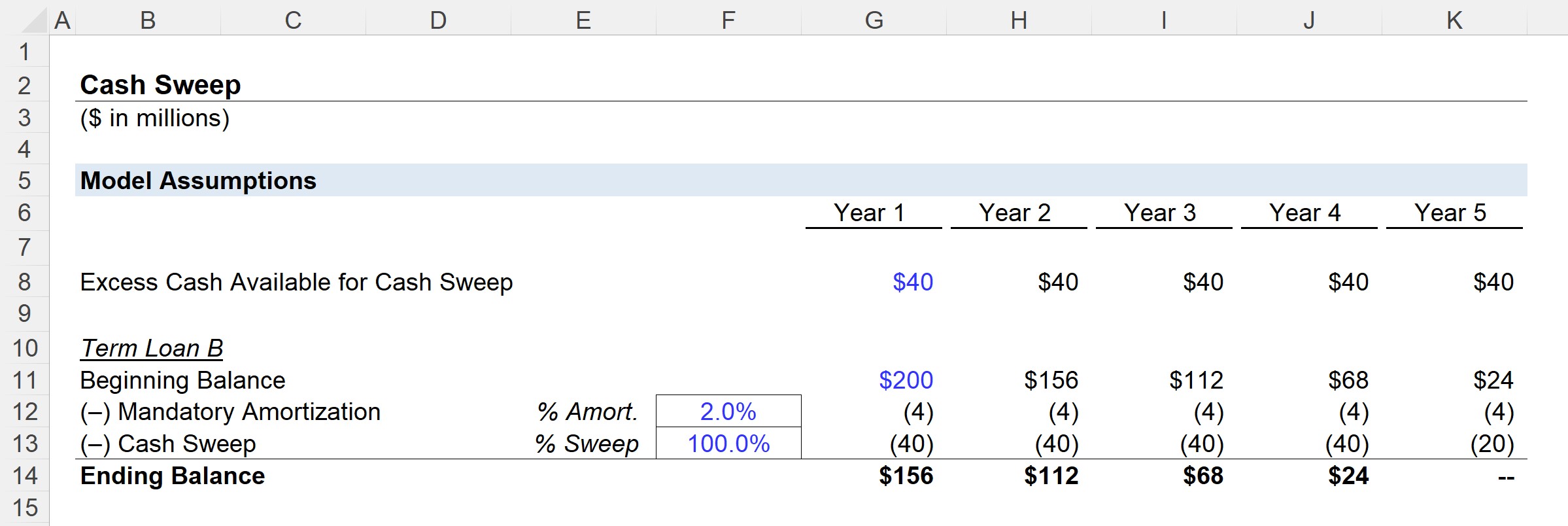

By the final year of the forecast, Year 5, note that the cash sweep amount is $20m. Since we have the “MIN” function in place to prevent the cash sweep from exceeding the sum of the beginning balance post-mandatory amortization, the cash sweep in Year 5 is $20m and the ending balance is zero.

")

Hi! Just a quick question on the topic! but if there is a minimum cash requirement that changes every year, do i need to consider it before the cash sweep right? I subtract this minimum amount from the FCF before cash sweep? or how do i model that out? Thanks… Read more »