- What is a 3-Statement Model?

- How to Build a 3-Statement Model

- How to Format the 3-Statement Financial Model

- What is Periodicity in 3-Statement Modeling?

- What is the Structure of a 3-Statement Model?

- Basic Elements of an Integrated 3-Statement Model

- SEC EDGAR: How to Gather Data for Financial Modeling?

- How to Forecast the Income Statement

- How to Forecast the Balance Sheet

- How to Forecast the Cash Flow Statement (CFS)

- How to Create Model Plugs? (Cash and Revolver)

- How to Handle a Circularity in Excel?

- How to Calculate Shares Outstanding and Earnings Per Share (EPS)

- How to Perform Scenario Analysis in Excel

- How to Conduct Sensitivity Analysis in Excel

- What Skills are Required in Financial Modeling?

- Why Does the 3-Statement Model Matter?

What is a 3-Statement Model?

The 3-Statement Model is an integrated model used to forecast the income statement, balance sheet, and cash flow statement of a company for purposes of projecting its forward-looking financial performance.

How to Build a 3-Statement Model

While accounting enables us to understand a company’s historical financial statements, forecasting those financial statements enables us to explore how a company will perform under various assumptions, and visualize how a company’s decisions interact to impact the bottom line in the future.

- Operating Decisions → i.e. “Let’s reduce prices”

- Investing Decisions → i.e. “Let’s buy an additional machine”.

- Financing Decisions → i.e. “Let’s borrow a bit more”.

A well-built 3-statement financial model helps insiders (corporate development professionals, FP&A professionals) and outsiders (institutional investors, sell side equity research, investment bankers and private equity) see how the various activities of a firm work together, making it easier to see how decisions impact the overall performance of a business.

How to Format the 3-Statement Financial Model

It is critical that a complex financial model like the 3-statement model adheres to consistent best practices. This makes both the task of modeling and auditing other people’s models far more transparent and useful.

We have written an Ultimate Guide to Financial Modeling Best Practices, but we’ll summarize some key takeaways here.

The most basic formatting rules are:

Color-code your model so that inputs are blue and formulas are black. The table below shows other color-coding best practices:

| Type of cells | Color |

|---|---|

| Hard-coded numbers (inputs) | Blue |

| Formulas (calculations) | Black |

| Links to other worksheets | Green |

| Links to other files | Red |

| Links to data providers (i.e. CIQ, FactSet) | Dark Red |

Format data consistently (for example, keep consistent unit scale, use 1 decimal place for numbers, 2 for per share data, 3 for share count).

Avoid partial inputs that commingle cell references with hard numbers.

Maintain standard column widths and consistent header labels.

What is Periodicity in 3-Statement Modeling?

One of the first decisions in building a 3-statement financial model concerns the periodicity of the model.

Namely, what are the shortest periods the model will be partitioned into annual, quarterly, monthly, or weekly?

This will typically be determined by the purpose of the 3-statement financial model.

Below we’ve outlined some general rules of thumb:

- Annual Models → Common when using the model to drive a DCF model valuation. This is because a DCF model needs at least 5 years of explicit forecasts before making terminal value. LBO models are often also annual models, as the investment horizon is around 5 years. An interesting wrinkle with annual models is the handling of the “stub period,” which captures the latest 3-, 6-, or 9-months of historical data).

- Quarterly Financial Models → Common in equity research, credit, financial planning and analysis, mergers and acquisitions (accretion/dilution) models where near-term issues are a catalyst. These models often roll up into an annual buildup.

- Monthly Financial Models → Common in restructurings and project finance where month-to-month liquidity tracking is critical. One thing to note is that the data required for a monthly buildup is usually unavailable to outside investors unless it is privately provided by management (companies typically don’t report monthly data). These models often roll up into a quarterly buildup.

- Weekly Financial Models → Common in bankruptcies. The most common weekly model is called the thirteen-week cash flow model (TWCF). The TWCF is a required submission in a bankruptcy process to track cash and liquidity.

What is the Structure of a 3-Statement Model?

When models get large, adhering to a strict structure is critical.

The key rules of thumb to follow include the following:

- Use roll-forward schedules when forecasting balance sheet items.

- Aggregate inputs in one worksheet or one section of the model and separate them from calculations and outputs.

- Avoid linking files together.

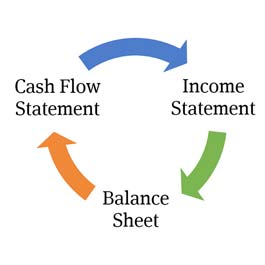

Basic Elements of an Integrated 3-Statement Model

An integrated 3-statement model

3-statement models include a variety of schedules and outputs, but the core elements of a 3-statement model are, as you may have guessed, the income statement, balance sheet, and cash flow statement.

A key feature of an effective model is that it is “integrated,” which simply means that the 3-statement models are modeled in a way that accurately captures the relationship and linkages between the various line items across the financial statements.

An integrated model is powerful because it enables the user to change an assumption in one part of the model to see how it impacts all other parts of the model consistently and accurately.

SEC EDGAR: How to Gather Data for Financial Modeling?

Before firing up Excel to begin building the model, analysts need to gather the relevant reports and disclosures.

At a minimum, they will need to gather the company’s latest SEC filings, press releases and possibly equity research reports.

Data is much harder to find for private companies than for public companies, and reporting requirements vary across countries. We have compiled a guide on gathering historical data needed for financial modeling here.

How to Forecast the Income Statement

The income statement illustrates a company’s profitability. All three statements are presented from left to right, with at least 3 years of historical results present to provide historical rations and growth rates on which forecasts are based.

Inputting the historical income statement data is the first step in building a 3-statement financial model.

The process involves either manual data entry from the given company’s 10K or press release or the use of an Excel plugin such as FactSet or Capital IQ to drop historical data directly into Excel.

Forecasting typically begins with a revenue forecast followed by the forecasting of various expenses. The net result is a forecast of the company’s income and earnings per share. The income statement covers a specified period such as a quarter or year.

For more on this, check out the complete income statement forecasting guide.

Income Statement Screenshot from the Wall Street Prep Premium Package Training Program

How to Forecast the Balance Sheet

Unlike the income statement, which shows operating results over a period of time (a year or a quarter), the balance sheet is a snapshot of the company at the end of the reporting period. The balance sheet shows the company’s resources (assets) and funding for those resources (liabilities and shareholder’s equity). Inputting historical balance sheet data is similar to inputting data in the income statement. The data is inputted either manually or through an Excel plugin.

In large part, the balance sheet is driven by the operating assumptions we make on the income statement. Revenues drive the operating assumptions in the income statement, and this continues to hold true in the balance sheet: Revenue and operating forecasts drive working capital items, capital expenditures, and a variety of other items. Think of the income statement as the horse and the balance sheet as the carriage. The income statement assumptions are driving the balance sheet forecasts.

Click here for a complete guide to forecasting the balance sheet

Balance Sheet Screenshot from the Wall Street Prep Premium Package Training Program

How to Forecast the Cash Flow Statement (CFS)

The final core element of the 3-statement model is the cash flow statement. Unlike on the income statement or the balance sheet, you aren’t actually forecasting anything explicitly on the cash flow statement and it isn’t necessary to input historical cash flow statement results before forecasting. That’s because the cash flow statement is a pure reconciliation of the year-over-year changes in the balance sheet.

Every individual line item on the cash flow statement should be referenced from elsewhere in the model (it should not be hardcoded) as it is a reconciliation. Constructing the cash flow statement correctly is critical to getting the balance sheet to balance.

Cash Flow Statement Screenshot from the Wall Street Prep Premium Package Training Program

How to Create Model Plugs? (Cash and Revolver)

A universal feature of a 3-statement model is that cash and a revolving credit line serve as model “plugs.” This simply means that a 3-statement model has an automatic way of ensuring that when the model projects a cash shortfall after all the line items are forecast, additional debt via a “revolver” account will automatically increase to finance the shortfall. Conversely, if the model projects a cash surplus, cash will accumulate by the amount of the surplus. While this seems fairly logical, modeling this can be tricky. Click here for a guide to forecasting the revolver and cash balance with a free excel template

How to Handle a Circularity in Excel?

Many financial models have to deal with a problem in Excel called circularity. A circularity in Excel occurs when one calculation either directly or indirectly depends on itself to arrive at an output. In the 3-statement model, a circularity can occur because of the model plugs described above. This makes Excel unstable and can create a variety of problems for those using the model. There are several elegant ways to deal with this issue. To learn more about how to deal with circularity, go to the “Circularity” section of our guide on financial modeling best practices.

How to Calculate Shares Outstanding and Earnings Per Share (EPS)

For public companies, projecting earnings per share is key. Forecasting the numerator of EPS is described in detail in our income statement forecasting guide, but forecasting shares outstanding can be done in a variety of ways, ranging from simply keeping the historical share count constant to a more sophisticated analysis that takes into account forecasts for share repurchases and issuances. Click here for a guide to forecasting EPS.

How to Perform Scenario Analysis in Excel

The purpose of building a 3-statement financial model is to observe how various operating, financing and investing assumptions impact a company’s forecasts. Once the initial case is built, it is useful to see — using either equity research, management guidance, or other assumptions — how the forecasts change given changes in a variety of key model assumptions. To this end, financial models often have a drop-down list that provides the user with the option to select either the original case (often called “base case”) or a variety of other scenarios (“strong case,” “weak case,” “management case,” etc.), which is referred to as scenario analysis.

How to Conduct Sensitivity Analysis in Excel

A close cousin of scenario analysis is sensitivity analysis. Any good 3-statement financial model (or a DCF model, LBO model, or M&A model, for that matter) will include the ability to toggle between various scenarios to see how the model’s outputs change, as well as something called sensitivity analysis. Sensitivity analysis is the process of isolating one (usually critical) model output to see how changes impact one or two key inputs.

For example, how would Apple’s 2020 EPS forecast change at various assumptions for 2020 revenue growth and gross profit margins? Click here to learn how to build a sensitivity analysis into a 3-statement model.

What Skills are Required in Financial Modeling?

Building a 3-statement financial model requires the combination of the following skills:

- Excel: Getting strong in Excel may seem daunting, but it’s actually the easiest skill on this list to develop. A general rule of thumb in finance is to avoid using the mouse and memorize some keyboard shortcuts. Accounting: This is the single most important (and least glamorous) part of getting strong in modeling. Understanding how the three financial statements are tied together and what each line item on the income statement, balance sheet and cash flow statement represents is the key to the conceptual understanding of how a 3-statement financial model works.

- Reading Financial Reports: Even though 3-statement financial models are designed to illuminate a firm’s future performance, setting up the model depends on a thorough understanding of what happened to the company in the past. For that, investment bankers and investors gather historical financial data. Whether you’re looking through SEC filings or quarterly press releases, or modeling a private company where you’re only provided piecemeal disclosures, finding the data you need will feel like a scavenger hunt. Your ability to navigate those reports and to find the exact data you are seeking can make a difference when building a model.

- Company and industry knowledge: One of the realities for new investment bankers is that they are often tasked with building a lot of models for industries and companies they don’t really know and don’t have time to learn. A 3-statement financial model’s assumptions about things like revenue growth and profit margins are critical to making a good forecast, so knowing the resources available to collect company and industry insights is very important. Quite often, investment bankers rely on sell side equity research to quickly get smart on the company and industry. Meanwhile, institutional investors (who, unlike investment bankers, have skin in the game) spend even more time getting to know the company, often through a lot of due diligence such as speaking with management and customers, going on-site visits, and trying out products themselves.

- Attention to detail: One wrong decimal place is all it takes to completely screw up a model. In investment banking, corporate finance, and equity research, the stakes are high and attention to detail is often the difference between getting promoted and getting fired.

Why Does the 3-Statement Model Matter?

At their core, all M&A, DCF, and LBO models depend on forecasts produced in the 3-statement model.

The output of a 3-statement model serves as the foundation for several types of financial models:

- Discounted Cash Flow (DCF) Modeling: In investment banking, private equity, and on the investment management side, practitioners value companies using a methodology called the DCF approach. This approach looks at a company’s future expected cash flows and discounts those cash flows to the present. While analysts sometimes rely on a “back of the envelope” approach when building the DCF, a rigorous DCF analysis requires a full 3-statement model to feed the cash flow forecasts.

- Mergers & Acquisitions (M&A) Modeling: To analyze the impact of an acquisition on a variety of key considerations for buyers and sellers, such as the acquirer’s profitability, accretion/dilution, capital structure, synergies post-acquisition, and the seller’s tax implications, 3-statement financial models for both companies need to be constructed and fused together.

- Leveraged Buyout (LBO) Modeling

The only way to truly understand how a leveraged buyout (or a management buyout) or a corporate bankruptcy or restructuring will impact a company’s performance (and thus ultimately determine the potential returns to the financial sponsors and lenders involved in the buyout), is to construct a 3-statement financial model for the buyout candidate, and it must be flexible enough to handle the new leveraged capital structure.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

Wonderful. I have a question. I have seen 3 statement model which is generated with the help of VBA bases macros. I guessed it needs some support files like simulation, forecasting assumptions etc to build a model. How to prepare these support files? Is it really required for modeling? Apart… Read more »

Please how do i include inflation rate in the financial model. How do I link them to the numbers in the model?