What is Trailing P/E Ratio?

The Trailing P/E Ratio is calculated by dividing a company’s current share price by its most recent reported earnings per share (EPS), i.e. the latest fiscal year EPS or the last twelve months (LTM) EPS.

How to Calculate Trailing P/E Ratio ?

The trailing price-to-earnings ratio is based on a company’s historical earnings per share (EPS) as reported in the latest period and is the most common variation of the P/E ratio.

If equity analysts are discussing the price-to-earnings ratio, it would be reasonable to assume that they are referring to the trailing price-to-earnings ratio.

The trailing P/E metric compares a company’s price as of the latest closing date to its most recently reported earnings per share (EPS).

The question answered by the trailing price-to-earnings is:

- “How much is the market willing to pay today for a dollar of a company’s current earnings?”

In general, the historical valuation ratios tend to be most practical for mature companies exhibiting low-single-digit growth.

Learn More → Valuation Multiple

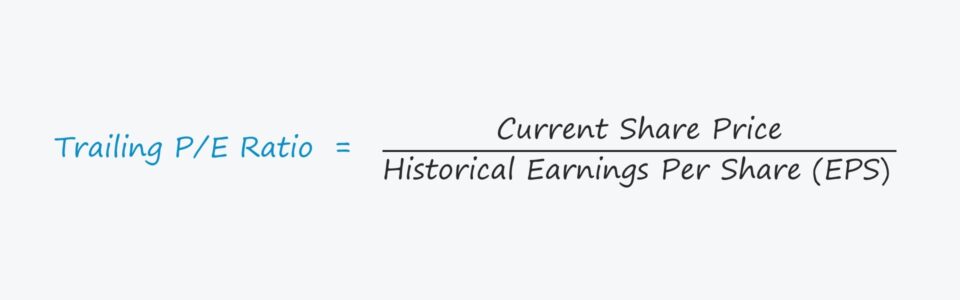

Trailing P/E Ratio Formula

Calculating the trailing P/E ratio involves dividing a company’s current share price by its historical earnings per share (EPS).

Where:

- Current Share Price: The current share price is the closing share price as of the latest trading date.

- Historical EPS: The historical EPS is the EPS value as announced in the latest fiscal year (10-K) or the latest LTM period based on the company’s most recent quarterly report (10-Q).

Trailing P/E Ratio vs. Forward P/E Ratio: What is the Difference?

The main benefit of using a trailing P/E ratio is that unlike the forward P/E ratio – which relies on forward-looking earnings estimates – the trailing variation is based on historical reported data from the company.

While there can be adjustments made that can cause the trailing P/E to differ between different equity analysts, the variance is much less than that of the forward-looking earnings estimates across different equity analysts.

Trailing P/E ratios are based on the reported financial statements of a company (“backward-looking”), not the subjective opinions of the market, which is prone to bias (“forward-looking”).

But sometimes, a forward P/E ratio can be more practical if a company’s future earnings reflect its true financial performance more accurately. For instance, a high-growth company’s profitability could change significantly in the upcoming periods, despite perhaps showing low-profit margins in current periods.

Unprofitable companies are unable to use the trailing P/E ratio because a negative ratio causes it to be meaningless. In such cases, the only option would be to use a forward multiple.

One drawback to trailing P/E ratios is that the financials of a company can be skewed by non-recurring items. In contrast, a forward P/E ratio would be adjusted to portray the normalized operating performance of the company.

Trailing P/E Ratio Calculator – Excel Template

We’ll now move to a modeling exercise, which you can access by filling out the form below.

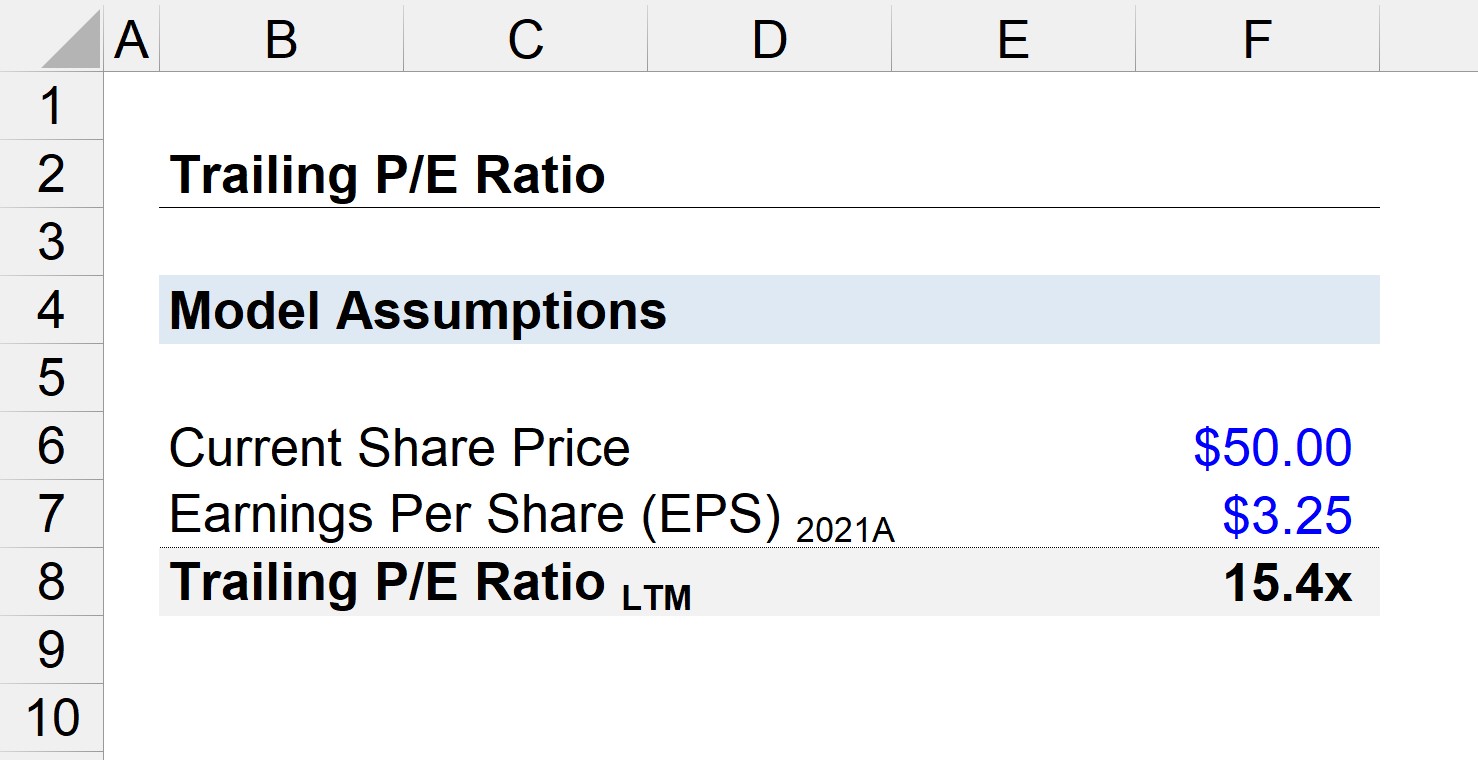

Trailing PE Ratio Calculation Example

Suppose a company’s latest closing share price was $50.00.

The most recent earnings report for the company was for its fiscal year 2021 performance, in which it announced earnings per share (EPS) of $3.25.

- Current Share Price = $50.00

- Earnings Per Share (EPS) = $3.25

Using those two assumptions, the trailing P/E ratio can be calculated by dividing the current share price by the historical EPS.

- Trailing P/E = $50.00 / $3.25 = 15.4x

The company’s P/E on a trailing basis is 15.4x, so investors are willing to pay $15.40 for a dollar of the company’s current earnings.

The 15.4x multiple would need to be compared against the company’s industry peers to determine if it is undervalued, fairly valued, or overvalued.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today