What is the Random Walk Theory?

The Random Walk Theory assumes price movements in the stock market are not predictable since they are determined by unexpected events with no correlation to the past.

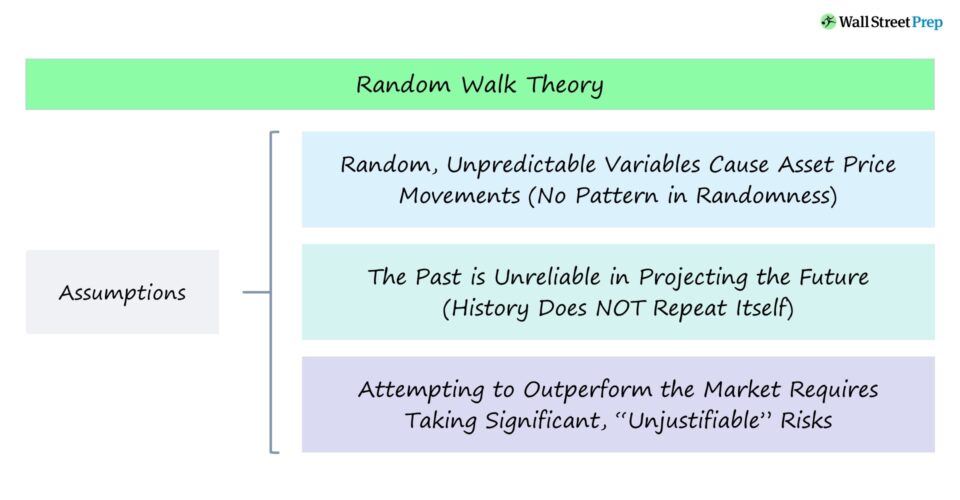

Random Walk Theory – Hypothesis Assumptions

The random walk theory states the prices reflected in the stock market are determined by random events independent of the past, i.e. there is no reliable orderly pattern.

In 1973, economist Burton Malkiel popularized the term in his book, A Random Walk Down Wall Street.

A “random walk” in probability theory refers to random variables impacting processes that are uncorrelated to past events and each other, i.e. there is no pattern to the randomness.

Historical data cannot be relied upon to reliably anticipate the future, which is contrary to the statement that “history repeats itself”.

Proponents of the random walk theory argue that forecasting is essentially pointless because for the models to be correct, they must accurately project random variables uncorrelated with the past.

If there were a pattern of fundamental or technical indicators, then the changes could be forecasted — but the random walk assumption claims otherwise.

Learn More → Hedge Fund Quick Primer

Random Walk Theory in Stock Market

The behavior of share price movements in the stock market is due to random, unpredictable events, according to the random walk theory.

The random walk assumption argues that attempts to predict share price movements accurately are futile, contrary to what active managers such as hedge funds claim.

Even if a decision were to be correct (and profitable) — regardless of the amount of fundamental or technical analysis used to support the decision — the positive outcome is more attributable to chance rather than actual skill.

Attempting to “beat the market” requires constantly taking on a substantial amount of “unjustifiable” risk because the outcome is a pure function of chance.

The Wharton Online & Wall Street Prep Applied Value Investing Certificate Program

Learn how institutional investors identify high-potential undervalued stocks. Enrollment is open for the Feb. 10 - Apr. 6 cohort.

Enroll TodayTrend of Passive Investing (ETFs + Mutual Funds)

The random walk theory recommends that the core of a portfolio should consist of index funds (i.e. passive “hands-off” investing), particularly for non-institutional retail investors.

Index funds are a form of passive investing and their widespread adoption was in part due to theories such as the random walk theory and active management being increasingly scrutinized and being neither worth the time (and effort) nor the fees.

The shift from active management to passive investing has benefited index funds such as the following investment vehicles:

Random Walk Theory vs. Efficient Market Hypothesis (EMH)

The random walk theory hypothesizes that share price movements are caused by random, unpredictable events.

For instance, the reaction of the market to unexpected events (and the resulting price impact) depends on how investors perceive the event, which is a random, unpredictable event too.

By contrast, the efficient market hypothesis (EMH) theorizes that asset prices reflect all information available in the market — which is classified into three distinct tiers.

- Weak Form EMH → All past information such as historical trading prices and data regarding volume is reflected in the market prices.

- Semi-Strong EMH → All public information available to all market participants is reflected in the current market prices.

- Strong Form EMH → All public and private information, even the knowledge of insiders, is reflected in the current market prices.

The random walk and efficient market theories are based upon different assumptions, yet arrive at virtually identical conclusions — i.e. it is near impossible to consistently outperform the market, which supports passive investing in lieu of active management strategies.

Criticism of Random Walk Theory

Under the efficient market hypothesis theory (EMH), market prices can neither be undervalued nor overvalued, as the market is assumed to be efficient.

The problem with the random walk theory is that if the market were hypothetically efficient, as proposed under EMH, then asset prices are rational (and fluctuations are not necessarily random).

Conversely, if the theory were in fact valid, the assumption negates the proposal of the EMH since it is implied that the market is irrational.

Another flaw within the theory is the assumption that the market corrects itself instantaneously once new information is made public.

But the issue here is that share prices can require time before stabilizing, especially for thinly traded securities.

The influence of unexpected events is undeniable, but there are also indeed recognizable trends and behavioral patterns among market participants that can directly impact share prices (e.g. momentum, overreaction).