- What is Market Volatility?

- How Does Stock Market Volatility Work?

- What Causes Volatility in the Stock Market?

- How Does Market Volatility Risk Impact Stock Prices?

- Realized vs. Implied Volatility (IV): What is the Difference?

- Which Factors Affect Volatility in Stocks?

- CBOE Volatility Index (VIX) – Stock Market Risk Indicator Example

What is Market Volatility?

Market Volatility describes the magnitude and frequency of pricing fluctuations in the stock market and is most often used by investors to gauge risk by helping to predict future price movements.

How Does Stock Market Volatility Work?

Volatility is the frequency and magnitude of the variance in the market pricing of an asset (or collection of assets).

Market volatility measures the frequency and magnitude of movements in asset prices – i.e. the size and rate of “swing-like” fluctuations.

Volatility is inherent to all asset values in the stock market and is a critical component of investing.

In the context of the stock market, volatility is the rate of fluctuations in a company’s share price (i.e. equity issuances) in the open markets.

The relationship between volatility and the perceived investment risk is the following:

- Higher Volatility → Riskier with Greater Potential for Losses

- Lower Volatility → Reduced Risk with Less Potential for Losses

If a company’s share price has historically undergone dramatic swings in pricing on a frequent basis, the stock would be considered to be volatile.

By contrast, if a company’s share price has remained stable with minimal deviation over time, the stock possesses low volatility, i.e. the share’s value does not fluctuate significantly or change frequently.

What Causes Volatility in the Stock Market?

The price of an asset is a function of supply and demand in the markets, so the root cause of volatility is uncertainty among investors.

Said differently, for volatile stocks, sellers are unsure where to set the asking price, and buyers are not certain what a reasonable bid price would be.

Furthermore, factors such as seasonality, cyclicality, market speculation, and unexpected events can affect the amount of uncertainty in the market.

- Seasonality: Regular seasonal changes tend to be more predictable since they are recurring, but share prices can still exhibit significant movements around important dates (e.g. retail companies and their holiday sales reports).

- Cyclicality: During different stages of the economic cycle, certain companies are more vulnerable to price movements (e.g. housing is prone to steep declines during recessions due to the exposure to new construction).

- Speculation-Driven: When a company’s value primarily stems from future earnings rather than existing earnings, its valuation is forward-looking – and changes in the prevailing market sentiment regarding future performance can cause significant price fluctuations (e.g. cryptocurrencies).

- Unexpected Events: Concerns about the future macro outlook aggravate the volatility of assets, often triggered by fear-inducing events such as a geopolitical conflict and sanctions, particularly for commodities (e.g. oil and the Russia/Ukraine conflict).

The Wharton Online & Wall Street Prep Applied Value Investing Certificate Program

Learn how institutional investors identify high-potential undervalued stocks. Enrollment is open for the Feb. 10 - Apr. 6 cohort.

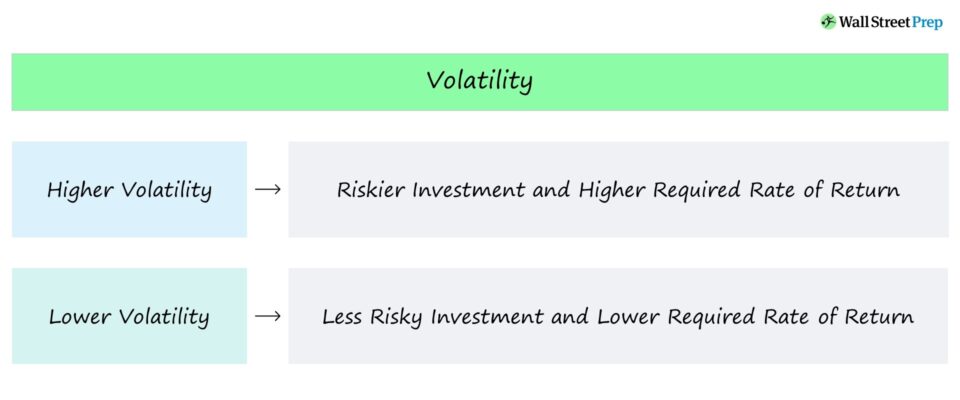

Enroll TodayHow Does Market Volatility Risk Impact Stock Prices?

The more volatile the price of a security, the riskier the investment is given the added unpredictability.

Investing is the act of balancing risk and reward, so the potential for outsized gains cannot exist without the possibility of incurring substantial losses.

If a company’s share price is constantly fluctuating, selling the investment for a profit (i.e. capital gain) requires “timing the market” properly and avoiding any unfavorable directional changes.

Otherwise, the investor could be forced to hold the investment for an extended period of time, which makes the stock a less attractive opportunity.

In effect, investors demand a higher rate of return to compensate for undertaking more uncertainty, i.e. a higher cost of equity.

- Higher Volatility → Riskier Investment and Higher Cost of Equity

- Lower Volatility → Less Risky Investment and Lower Cost of Equity

Learn More → Hedge Fund Quick Primer

Realized vs. Implied Volatility (IV): What is the Difference?

Volatility can be separated into two distinct measures:

- Historical Volatility: Often used interchangeably with “realized volatility,” the measure is calculated using historical prices to predict future market volatility.

- Implied Volatility (IV): On the other hand, implied volatility is a “forward-looking” calculation using data on derivative instruments, namely S&P 500 options, to estimate future market volatility.

In practice, implied volatility (IV) holds more weight than historical volatility due to being a forward-looking rather than a backward-looking statistical gauge calculated from past price changes.

The implied volatility in the broader market can be affected by events such as

- Global Recession Fears

- Presidential Elections

- Geopolitical Conflict

- Pandemics / Crisis

- Regulatory Policy Changes

Which Factors Affect Volatility in Stocks?

In valuation, one common measure of volatility is called “beta (β)” – which is defined as the sensitivity of a security (or portfolio of securities) to systematic risk relative to the broader market.

Most practitioners use the S&P 500 as the proxy market return to compare against a particular company’s stock price data.

The difference between systematic and unsystematic risk is explained below:

- Systematic Risk → Often called “market risk,” systematic risk is inherent to the public equities market rather than impacting one specific company or industry – so systematic risk cannot be mitigated through portfolio diversification (e.g. global recession, COVID pandemic).

- Unsystematic Risk → Conversely, unsystematic risk (or “company-specific risk”) pertains only to a specific company or industry – unlike systematic risk, it can be mitigated through portfolio diversification (e.g. supply chain disruption).

Beta depicts the correlation between a particular stock’s price and the S&P 500 (“the market”), which is interpreted using the following guidelines.

- Beta = 1.0 → No Market Sensitivity

- Beta > 1.0 → High Market Sensitivity (i.e. More Risk)

- Beta < 1.0 → Less Market Sensitivity (i.e. Less Risk)

Implied Volatility (IV) vs. Beta

The implied volatility and beta are both measurements of a stock’s volatility.

- The implied volatility is based on “forward-looking” investor sentiment surrounding future price movements.

- Beta, on the other hand, is “backward-looking” and compares a stock price’s historical changes to changes in the broader market.

CBOE Volatility Index (VIX) – Stock Market Risk Indicator Example

Uncertainty results in more volatility, and the prevailing market sentiment emerges in the prices of speculative financial instruments.

The Chicago Board Options Exchange (CBOE) created the Volatility Index (VIX) in 1993.

Since then, the VIX is one of the most frequently used to gauge market volatility and investor sentiment by market participants such as traders and investors.

The VIX estimates the S&P’s implied volatility by looking at the prices of options on the underlying equities tracked within a 30-day time frame, which is then annualized to determine a formal prediction.

The implied volatility attempts to quantify the volatility expectations by options traders (i.e. put and call options) – hence, the VIX is often referred to as the “fear index.”

Often, if the VIX is high, the stock prices in the market fall, and investors allocate more of their capital to fixed-income securities (e.g. treasury bonds, corporate bonds) and “safe havens” like gold.

CBOE VIX Chart

For example, the impact of the COVID pandemic in early 2020 (i.e. the sudden spike) can clearly be seen in the VIX chart below.

CBOE VIX Chart (Source: CNBC)

Leading up to a company’s earnings report, the implied volatility tends to increase substantially (i.e. options activity and variance), especially for high-growth equities.

The implied volatility can be derived by looking at the pricing of options, with the general rules of thumb listed below:

- If options prices have risen, investors are implied to be expecting sharp movements in prices.

- If options prices have declined, investors are implied to be expecting fewer movements in prices.

Volatility is not inherently a negative sign for investors, but investors must still understand that the potential for outsized returns comes at the cost of incurring significant losses.