What is Fixed Interest Rate?

A Fixed Interest Rate remains constant for the entirety of the loan agreement, as opposed to being tied to a prime rate or underlying index.

How to Calculate Fixed Interest Rate

If a loan or bond is priced at a fixed interest rate, the interest rate – which determines the interest expense amount due each period – is fixed and does not fluctuate over time.

In general, fixed pricing tend to be more prevalent with bonds and riskier debt instruments further down in the capital structure, rather than senior debt provided by banks.

The distinct benefit of fixed rates is the predictability in the pricing of the debt, as the borrower does not need to be concerned about changing market conditions that may impact the interest due.

The fact that the interest rate pricing structure is fixed mitigates any risk that the borrower’s interest expense payments could increase substantially.

Typically, borrowers are more likely to opt for fixed rates in lending agreements during low interest rate environments in an attempt to “lock-in” favorable borrowing terms for the long term.

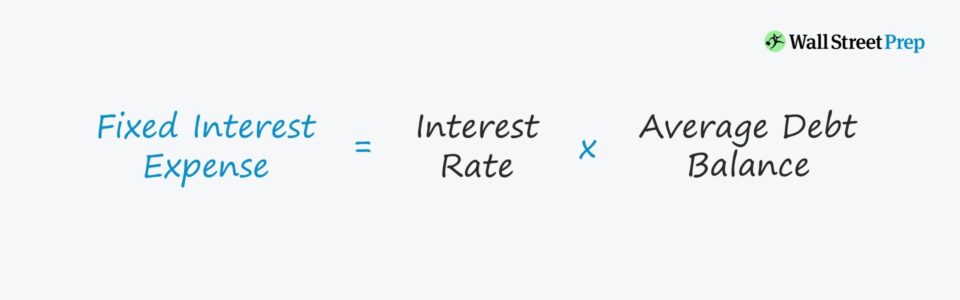

Fixed Interest Rate Formula

The formula for calculating the interest expense on a debt instrument with fixed pricing is as follows.

Fixed Interest Rate vs. Floating Interest Rate: What is the Difference?

Unlike fixed pricing rates, floating rates fluctuate based on the underlying benchmark rate that is tied to the pricing of the debt (e.g. LIBOR, SOFR).

The relationship between the market rate and the yield on debt priced at a floating rate is as follows.

- Declining Market Rate: If the market rate declines, the borrower benefits from the lower interest rate.

- Rising Market Rate: If the market rate rises, the lender benefits from the higher interest rate.

Floating interest rates thus can be a riskier form of debt pricing with more uncertainty because of the unpredictable changes in the underlying benchmark.

If the debt is priced on a fixed basis, the original interest rate remains the same, which eliminates any concerns from the borrower regarding how much interest will be owed.

However, the fixed pricing comes at the expense of not being able to benefit in lower interest rate environments.

For example, if the benchmark rate is lower and the lending environment becomes more favorable for borrowers, interest expense on a bond priced at a fixed rate would still stay unchanged.

Fixed Interest Rate Calculator

We’ll now move to a modeling exercise, which you can access by filling out the form below.

Fixed Interest Rate Calculation Example

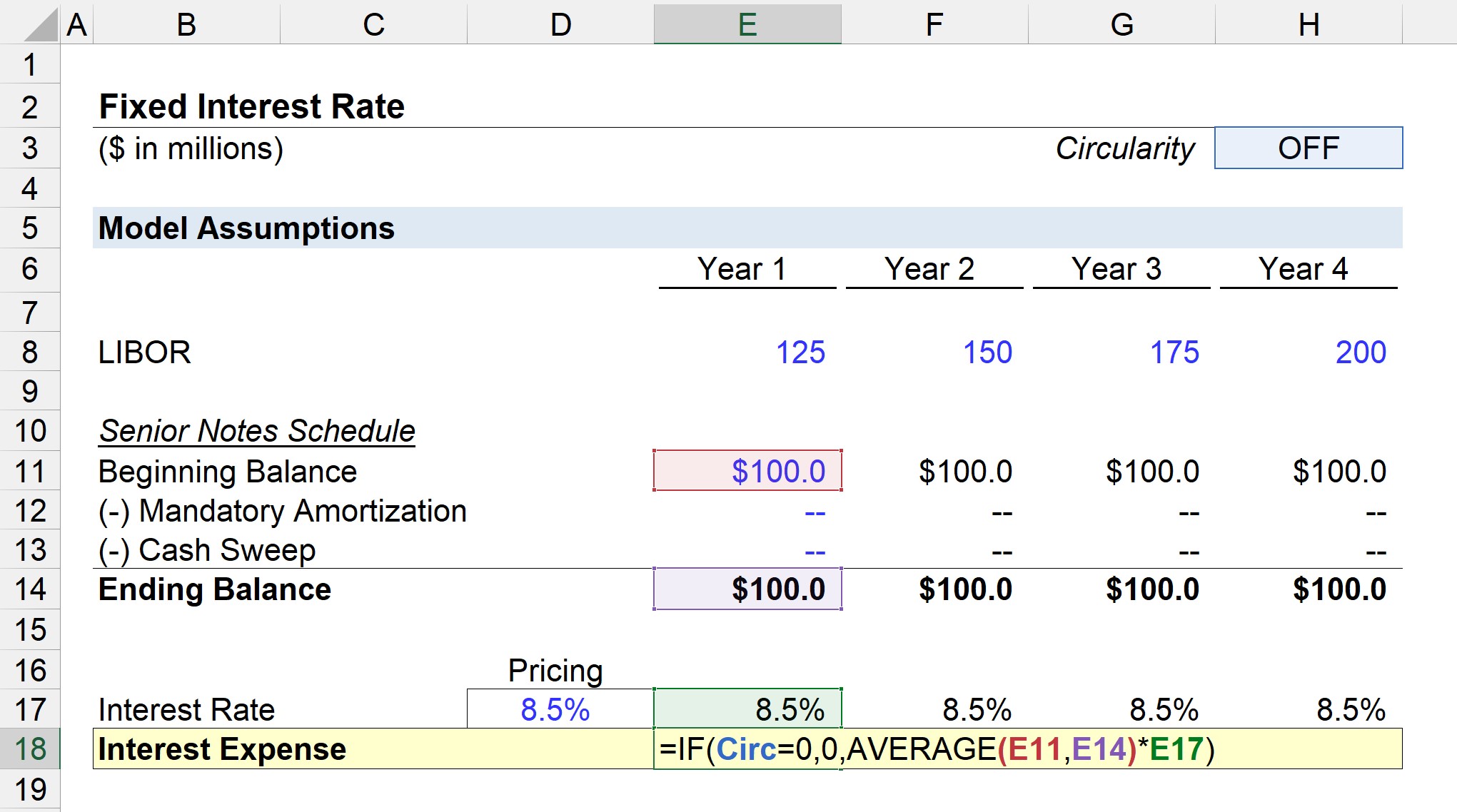

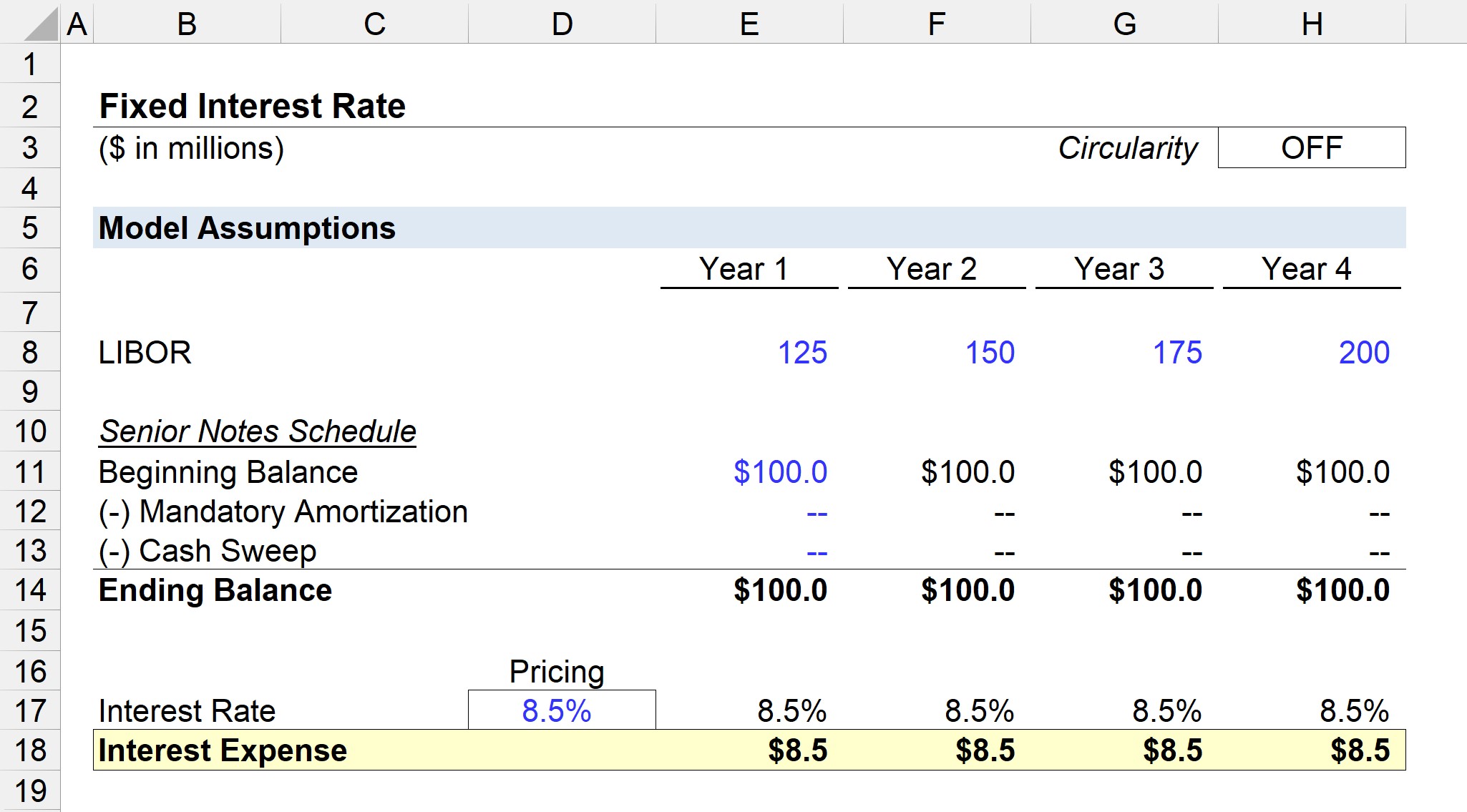

In our illustrative example, we’ll assume there is a senior note with a total outstanding balance of $100 million.

For the sake of simplicity, there’ll be no mandatory amortization or cash sweeps (i.e. optional prepayments) across the forecast period.

- Senior Notes, Beginning Balance = $100 million

- Mandatory Amortization = $0

- Cash Sweep = $0

For a variable interest rate, a spread is added to the market rate (e.g. LIBOR) for each corresponding year.

LIBOR Curve

- Year 1 = 125 bps

- Year 2 = 150 bps

- Year 3 = 175 bps

- Year 4 = 200 bps

But in this case, the senior notes are priced at a fixed rate of 8.5%, which is kept constant for the entirety of the forecast and multiplied by the average between the beginning and ending balance.

- Interest Rate, % = 8.5%

While not relevant to our scenario because of our assumption of no mandatory amortization or cash sweep, we must add a circularity switch to offset the risk of our model malfunctioning due to the circularity created.

If the “Circ” cell is set to zero, the output is zero. But if the “Circ” cell is NOT set to zero, the output is the calculated expense using the beginning and ending balance of the company’s senior notes.

Since the balance of the senior notes does not change at all throughout the four years, the interest expense stays at $8.5 million every year, as shown below.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today