What are Accrued Expenses?

Accrued Expenses refer to a company’s incurred expenses related to employee wages or utilities yet to be paid off in cash, which is often attributable to the invoice not yet being received.

- Accrued expenses describe the costs incurred by a company that have not yet been paid for.

- Accrued expenses are recognized on the current liabilities section of the balance sheet.

- Accrued expenses are recorded on the income statement to abide by the matching principle of accrual accounting, even if there was no transfer of cash.

- Common examples of accrued expenses include wages, utilities, and services received but not yet invoiced.

- Accrued expenses have a net positive impact on a company’s free cash flow (FCF) until paid off.

- The accounting entry for an accrued expense consists of debiting the expense account and crediting the accrued liability account, reflecting the obligation to pay in the future (“cash outflow”).

How are Accrued Expenses Created?

On the current liabilities section of the balance sheet, a line item that frequently appears is “Accrued Expenses,” also known as accrued liabilities.

An accrued liability is an expense that has been incurred — i.e. recognized on the income statement — but has not actually been paid yet.

Per the “matching principle” under accrual accounting, the benefit associated with the expense dictates when the expense appears on the books of the company.

Despite the fact that the cash outflow has not occurred, the expense is recorded in the reporting period incurred.

Similar to accounts payable, accrued expenses are future obligations for cash payments to soon be fulfilled; hence, both are categorized as liabilities.

Accrued Expenses: Examples on Balance Sheet

For example, let’s say that a company’s employees are paid bi-weekly and the starting date is near the end of the month in December.

The benefit of the employees working was received, so the expense is recognized in December, but the employees may not receive cash compensation until the following month, early January.

As a result, the accrued expense balance increases from the unpaid employee wages caused by the timing mismatch.

Examples of Accrued Expenses

- Payroll (i.e. Salaries)

- Utility Bills (HVAC)

- Rent

- Accrued Interest

- Accrued Taxes

Accrued Expense Journal Entry: Debit or Credit

If an accrued expense is incurred and recognized, the initial journal entry is as follows.

- Employee Payroll Account ➝ Debit

- Accrued Wages ➝ Credit

For example, suppose we’re accounting for an accrued rental expense of $10,000.

The initial journal entry on the company’s books is as follows.

| Journal Entry | Debit | Credit |

|---|---|---|

| Rental Expense | $10,000 | |

| Accrued Rental Expense | $10,000 |

The entry reverses at the beginning of the following reporting period, assuming the company follows through with the payment on time.

| Journal Entry | Debit | Credit |

|---|---|---|

| Accrued Rental Expense | $10,000 | |

| Rental Expense | $10,000 |

How Do Accrued Expenses Impact Free Cash Flow (FCF)

Simply put, more accrued expenses are created when goods/services are received, but the cash payment remains in the possession of the company.

Oftentimes, the reasoning for the delayed payment is unintentional but rather due to the bill (i.e. customer invoice) having not been processed and sent by the vendor yet.

The rules regarding the impact on free cash flow (FCF) are as follows:

- Increase in Accrued Liabilities → Positive Impact on Cash Flows

- Decrease in Accrued Liabilities → Negative Impact on Cash Flows

The intuition is that if the accrued liabilities balance increases, the company has more liquidity (i.e. cash on hand) since the cash payment has not yet been met.

By contrast, a decrease in the accrued liabilities balance means the company fulfilled the cash payment obligation, which causes the balance to decline.

Accrued Expenses Calculator

We’ll now move to a modeling exercise, which you can access by filling out the form below.

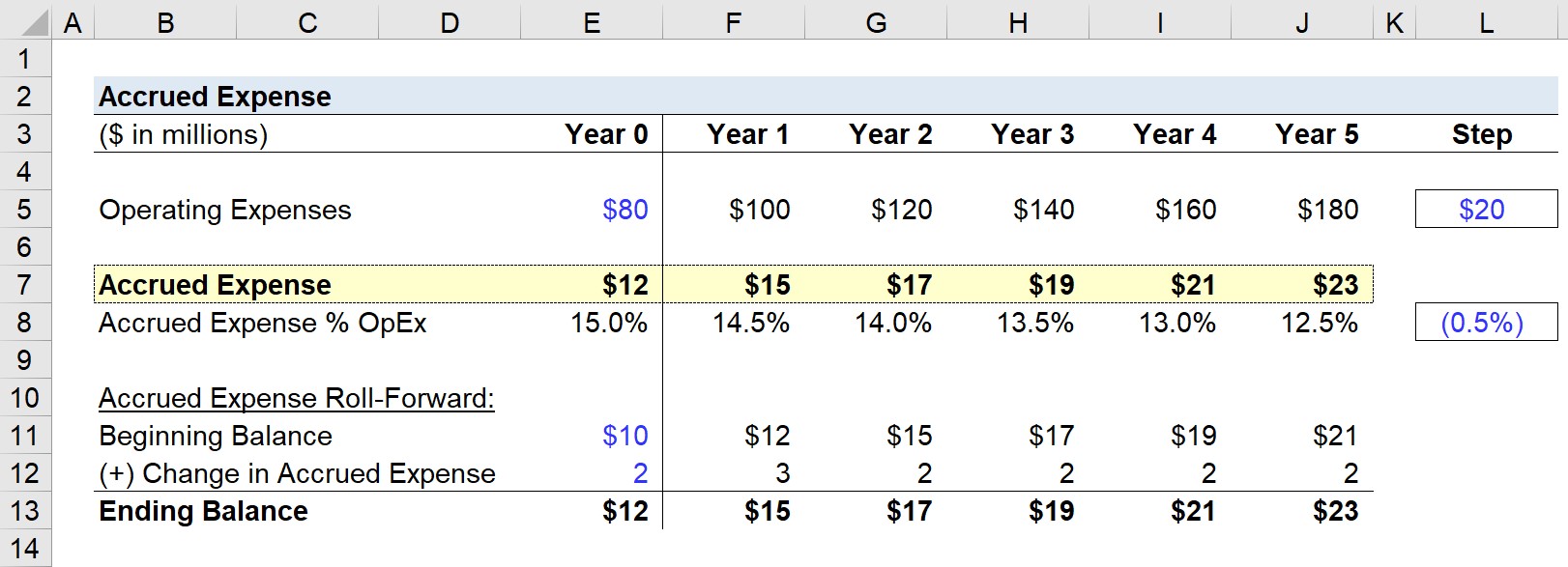

Accrued Expenses Calculation Example

Most often, a company’s accrued expenses are closely aligned with operating expenses (e.g. rent, utilities).

With that said, the standard modeling convention for modeling the current liability is as a percentage of operating expenses (OpEx) — i.e. the growth is tied to the growth in OpEx.

However, if the amount of the expense is negligible, the account can be combined with accounts payable (A/P) or projected to grow in line with revenue growth.

Here, we’ll be projecting the expense as a % of operating expenses.

The following assumptions will be used in our model.

Year 0 Financials:

- Operating Expenses (OpEx) = $80 million (Increase by $20 Each Year)

- Accrued Expenses = $12m (Decline by 0.5% as Percentage of OpEx Each Year)

In Year 0, our historical period, we can calculate the driver as:

- Accrued Expenses % of OpEx (Year 0) = $12 million ÷ $80 million = 15.0%

Then, for the forecast period, the accrued expenses will be equal to the % OpEx assumption multiplied by the matching period OpEx.

From Year 0 to Year 5, our assumption declines from 15.0% to 12.5%, and the following change occurs in the projected values:

- Year 0 to Year 5: $12 million ➝ $23 million

In closing, our model’s roll-forward schedule captures the change in accrued expenses, and the ending balance flows into the current period balance sheet.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today