- What is the Risk Free Rate?

- How to Calculate Risk Free Rate (rf)

- Risk Free Rate Formula (rf)

- What is the Role of the Risk Free Rate in CAPM?

- How Does the Risk-Free Rate Affect Discount Rate?

- What is the Impact of Rising Risk-Free Rate on Valuation?

- What is Normalized Cost of Capital?

- Risk Free Rate Calculator — Excel Template

- 1. Real Risk Free Rate and Inflation Rate Assumptions

- 2. Nominal Risk Free Rate Calculation Example

What is the Risk Free Rate?

The Risk Free Rate (rf) is the theoretical rate of return received on zero-risk assets, which serves as the minimum return required on riskier investments. The risk-free rate should reflect the yield to maturity (YTM) on default-free government bonds of equivalent maturity as the duration of the projected cash flows.

How to Calculate Risk Free Rate (rf)

For corporate valuations, the majority of risk/return models begin with the presumption that there is a so-called “risk-free rate”.

The yield on a risk-free asset – most commonly the 10-year Treasury bond in the US – is the minimum rate of return expected on investments with “zero risk” and the starting point upon which many valuation models build.

Despite the fact that the return expected by investors is considered to be risk-free, it is important to remember that the risk-free rate is a mere simplification, as all investments carry some degree of risk.

However, government-issued bonds are logically about as close to being risk-free as an asset could get, as governments could simply print more money if necessary.

As a result of being secured by a central government, the probability of default on such bond issuances is practically zero – and therefore, government bonds are viewed as the safest asset class that investors could place their capital in.

The risk-free rate should ideally match the duration of the forecast period of the cash flows, however, the limited liquidity and data for the longest maturity government-issued bonds have made the current yield on 10-year US treasury notes the preferred risk-free rate proxy in the U.S.

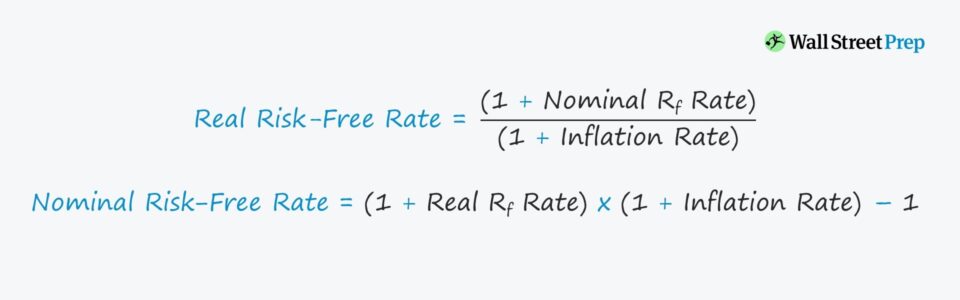

Risk Free Rate Formula (rf)

To expand further on the risk-free rate, there are two different types to consider:

- Real Risk-Free Rate

- Nominal Risk-Free Rate

The reasoning behind these two concepts is related to the inclusion (or exclusion) of the rate of inflation.

The real risk-free rate is the required return on zero-risk financial instruments with the rate of inflation taken into account.

The relationship between the real and the nominal risk-free rate is depicted by the following equation:

The nominal risk-free rate refers to the yield on a risk-free asset without the effect of inflation.

If the projected cash flows are discounted in nominal terms (i.e. reflects expected inflation), the discount rate used should also be nominal.

What is the Role of the Risk Free Rate in CAPM?

The risk-free rate has a significant role in the capital asset pricing model (CAPM), which is the most widely used model for estimating the cost of equity.

Under the CAPM, the expected return on a risky asset is estimated as the risk-free rate plus an approximated equity risk premium. The minimum threshold for return factors in the beta of the specific asset (i.e. systematic risk) and the average return of the stock market.

The risk-free rate serves as the minimum rate of return, to which the excess return (i.e. the beta multiplied by the equity risk premium) is added.

The equity risk premium (ERP) is calculated as the average market return (S&P 500) minus the risk-free rate.

The equity risk premium helps investors evaluate potential investments based on the “extra” return that they are receiving for the incremental risk above the rf rate.

In effect, the risk-free rate has broad implications on how investors allocate their capital based on prevailing market conditions.

LIBOR to SOFR Transition

LIBOR, the standard benchmark used in the financial markets for setting interest rates on loans and various debt instruments, is being phased out and replaced by SOFR by the end of 2021.

How Does the Risk-Free Rate Affect Discount Rate?

The risk-free rate assumption is also a key input in the estimation of the weighted average cost of capital (WACC) of a company.

The CAPM estimates the cost of equity based on the risk-free rate of return and the additional risk (and required return) associated with the investment. But the cost of debt can also be estimated by adding a certain spread based on the risk profile (i.e. default risk premium) of the company to the risk-free rate.

If the risk-free rate increases, there will be increased pressure on the equity risk premium to compensate investors more for the amount of risk undertaken (and vice versa).

Since investors can receive higher returns from risk-free assets, riskier assets are expected to result in higher returns to meet the new standards set by the market for the returns of riskier assets.

All else being equal, lower risk-free rates result in lower discount rates, which directly causes higher valuations of equities.

What is the Impact of Rising Risk-Free Rate on Valuation?

There are various theories as to why the markets rebounded rather quickly after bottoming around March 2020, but one reason behind the rapid recovery is the role of the risk-free rate.

Around this particular time, when the market declined significantly due to the uncertainty surrounding COVID-19, the U.S. 10-year treasury notes ranged from around 0.6% to 0.8%.

Institutional and retail investors were left with two choices:

- Government Bonds: Invest in risk-free government bonds yielding practically nothing (<1.0%) – with the Fed indicating no plans for interest rate hikes until the economy reached full recovery.

- Blue Chip Stocks: Invest in the largest, market-leading companies, most notably the “FANG” stocks (Facebook, Amazon, Apple, Netflix, and Google), which each had a significant likelihood of enduring through this period – if not even benefiting from the lockdown period.

The performance of the stock market makes it clear which decision many investors chose, especially for the tech giants that saw a disproportionate outperformance relative to the broader market as they led the market’s swift recovery (and the eventual surpassing of record all-time highs).

What is Normalized Cost of Capital?

If the prevailing interest rates in the market are at historically low levels, DCF-derived valuations tend to be higher since the discount rate is going to be lower from the decline in the risk-free rate.

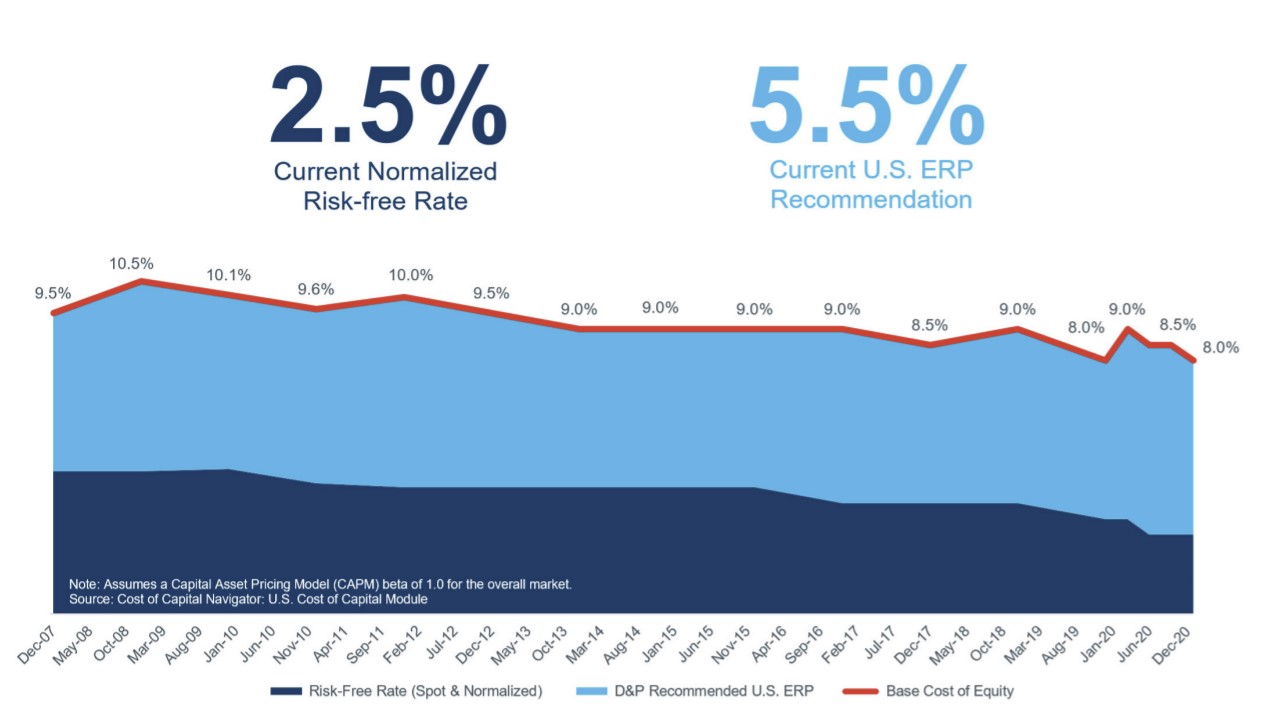

There has been much debate on normalized risk-free rates, with Duff & Phelps regularly publishing reports on their recommended equity risk premium (ERP), which uses a normalized version of the risk-free rate.

Duff & Phelps Recommended Equity Risk Premium (Source: Duff & Phelps)

Conversely, NYU Professor Aswath Damodaran has argued against the use of normalized rates, stating that the rf rate should reflect the real opportunity cost – i.e. the actual options available – as of the present date.

Damodaran on Normalized Risk Free Rates (Source: Damodaran – Musings on Markets)

Damodaran on Normalized Risk Free Rates (Source: Damodaran – Musings on Markets)

Risk Free Rate Calculator — Excel Template

We’ll now move to a modeling exercise, which you can access by filling out the form below.

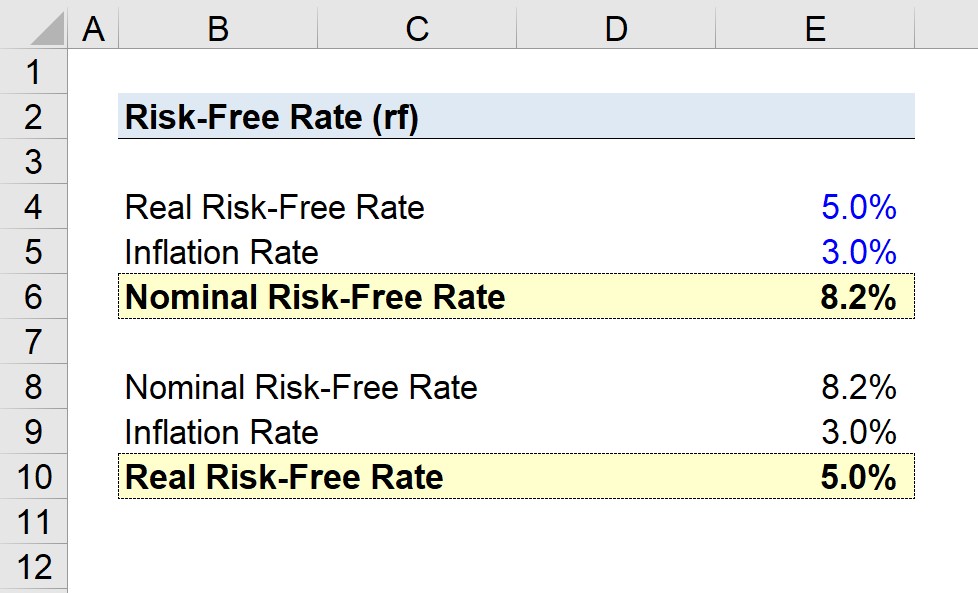

1. Real Risk Free Rate and Inflation Rate Assumptions

For our risk-free rate modeling exercise, we’ll first calculate the nominal risk-free rate and then move to the real risk-free rate.

- Real rf Rate = 5.0%

- Inflation Rate = 3.0%

2. Nominal Risk Free Rate Calculation Example

From those two assumptions, we’ll enter them into the formula to calculate the nominal risk-free rate:

- Nominal rf Rate = (1 + 5.0%) × (1 + 3.0%) – 1

Here, the nominal risk-free rate comes out to 8.2%.

Next, we’ll calculate the real risk-free rate using the same assumptions to confirm our calculation is correct.

- Real rf Rate = (1 + 8.2%) ÷ (1 + 3.0%) – 1

As expected, we arrive at 5.0% for our real risk-free rate, which is the rate of return on the risk-free security once adjusted for the impact of inflation.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

")

")

")